Episode 37: 보험회사에 대해 알아보자.

실제로 상조회에서 출발한 보험회사를 운영하는 데에는 몇 가지 원칙이 있습니다. 이 원칙들을 보면 보험회사에 대한 편견이 얼마나 심각하게 우리의 삶을 힘들게 할 수 있는 지 알 수 있는 잣대가 될 것입니다.

보험회사의 운영 원칙

보험회사는 보험상품을 만들 때 아래의 세 가지 조건에 따라 만들게 됩니다.

첫째는 수지상등(收支相等)의 원칙입니다.

보험회사의 수입과 지출은 서로 같아야 한다는 원칙입니다.

보험회사는 고객이 내는 보험료에서 회사가 운영비용으로 쓰는 부가보험료를 제외한 나머지를 운용해서 보험금을 지급하거나 만기에 환급금을 지급해야 합니다. 이 과정에서 발생한 이익은 전액 고객에게 돌려주어야 한다는 원칙(배당부 보험의 조건)을 가지고 있습니다.

둘째는 경험생명표의 적용입니다.

보험회사가 일정한 기간 동안 보험금을 지급한 경험을 기준으로 사람의 수명을 예측하는 통계표로서 회사는 이를 기초로 나이와 성별, 건강 등에 따라 보험료를 차등 적용하게 됩니다. 젊은 사람들은 보험금을 늦게 받을 확률이 높으므로 비교적 저렴한 보험료를 오랫동안 내게 하고, 사망확률이 높은 사람들은 비교적 많은 보험료를 짧은 기간 동안 내게 하는 것입니다.

통상 우리나라의 경우 여성이 남성보다 더 오래 살기 때문에 동일한 보장(보험금)이라면 여성의 보험료가 남성보다 저렴하며 흡연자 보다는 비흡연자의 보험료가 저렴합니다. 그러나 오래 살든 아니든 확률적으로 고객이 납입하는 총 보험료의 규모는 지급되는 보험금과 동일하게 되도록 가정하여 보험료를 산출합니다.

셋째는 대수의 법칙(大數의 法則)입니다.

특수한 상황의 몇몇이 가입하는 것이 아니라 다양한 연령과 성별의 많은 사람들이 가입하는 것을 가정하여 사망률 등의 통계에 대한 오차를 줄이려는 기준입니다.

이렇게 보험회사는 고객이 총무에게 주기로 약속한 부가보험료 외의 이익을 취할 수 없는 회사이며 누가 보아도 이해할 수 있을 만큼 아름다운 생각으로 시작한 회사입니다. 그런데 이렇게 아름다운 상조회의 모습을 그대로 갖추고 있는 보험회사가 왜 많은 사람에게 욕을 먹고 있는 것일까요?

그것은 바로 회원도 그리고 총무도 실제 보험의 본질을 잘못 이해하고 있기 때문입니다.

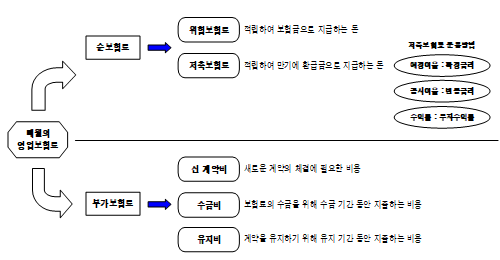

보험료의 구조

모든 보험상품의 보험료(고객이 납입하는 돈)는 순보험료와 부가보험료로 나뉩니다. 부가보험료는 고객이 총무에게 주는 급여이고, 보험료 대비 일정 비율로 책정됩니다.

순보험료는 다시 위험보험료와 저축보험료로 구분이 되는데, 위험보험료는 가입한 고객에게 보험금으로 지급하기 위해 모아두는 돈이고 저축보험료는 고객의 보험이 만기가 되었을 때 지급하기 위해 모아두는 돈입니다.

보험회사는 고객이 납입한 보험료에서 부가보험료를 받아 운영비로 사용하고, 순보험료는 따로 적립해 두었다가 보험금으로 지급하거나 환급금으로 돌려주게 됩니다.

따라서 보험료를 납입하면 부가보험료는 회사가 사용하게 되지만, 고객은 가입기간 중에 사고가 발생할 경우 보험금을, 계약이 종료된 후에는 적립된 만기 환급금을 받게 됩니다.

그런데 순보험료 중 위험보험료는 다른 고객이 낸 위험보험료와 함께 보험금으로 지급되기 때문에 계약이 종료되면(만기가 되면) 통상 돌려받을 수 없는 돈입니다.

따라서 부가보험료와 위험보험료는 일반적으로 소멸되는 금액이란 이야기지요. (계속)

—————-

Episode 37: Understanding Insurance Companies

In practice, there are several fundamental principles involved in operating an insurance company that originated from a mutual aid association. Examining these principles provides a clear standard for understanding how misconceptions about insurance companies can seriously impact our lives.

Principles of Insurance Company Operations

When insurance companies design insurance products, they follow three key principles.

First is the principle of equivalence of income and expenditure.

This principle states that the income and expenses of an insurance company must be balanced. Insurance companies must manage the portion of premiums paid by customers—excluding the loading premium used for operational expenses—in order to pay out insurance claims or maturity benefits. Any profit generated in this process must be fully returned to policyholders, which is a condition applied to participating insurance policies.

Second is the application of the mortality table based on experience.

This is a statistical table used to predict human life expectancy based on an insurance company’s past experience of claim payouts over a certain period. Based on this, premiums are applied differently depending on factors such as age, gender, and health condition. Younger individuals are likely to receive insurance payouts later, so they pay relatively lower premiums over a longer period, while individuals with a higher probability of death pay relatively higher premiums over a shorter period.

In general, in Korea, women tend to live longer than men. Therefore, for the same level of coverage, women’s premiums are lower than men’s, and non-smokers pay lower premiums than smokers. However, regardless of longevity, premiums are calculated under the assumption that the total amount paid by customers will, probabilistically, equal the total insurance payouts.

Third is the law of large numbers.

This principle assumes that not just a few individuals in special circumstances, but a large and diverse group of people across different ages and genders will subscribe, thereby reducing statistical errors such as mortality rates.

Thus, an insurance company is structured in a way that it cannot generate profit beyond the loading premium that customers agree to pay for operational expenses. It is a system founded on a concept that is, by all accounts, quite rational and well-intentioned. So why do insurance companies, which maintain the original structure of mutual aid associations, receive so much criticism?

The reason lies in the fact that both policyholders and administrators often misunderstand the true nature of insurance.

Structure of Insurance Premiums

All insurance premiums (the money paid by customers) are divided into net premiums and loading premiums. The loading premium represents compensation paid to the insurer for administrative costs and is calculated as a certain percentage of the total premium.

The net premium is further divided into risk premium and savings premium. The risk premium is the portion reserved to pay insurance claims, while the savings premium is accumulated to be returned to the policyholder at the maturity of the policy.

Insurance companies use the loading premium from customer payments as operational expenses, while the net premium is separately reserved and later used to pay insurance benefits or returned as maturity refunds.

Therefore, when premiums are paid, the loading premium is used by the company, but the customer receives insurance benefits in the event of an incident during the policy period, or the accumulated maturity refund after the contract ends.

However, the risk premium within the net premium is pooled with the risk premiums of other policyholders and used for claim payments. As a result, when the contract ends (at maturity), this portion is typically not refundable.

Thus, both the loading premium and the risk premium are generally considered extinguished amounts. (To be continued)