사람의 일생과 경제적 가치

보장이란 영어로 쓰면 Protection입니다. 보호한다는 이야기입니다. 그럼 무엇으로부터 보호받아야 하는 걸까요? 너무 일찍 죽거나 너무 오래 사는 것으로부터 보호받아야 한다고들 이야기하지만, 책에 나온 이야기 말고 없는 이야기를 한 번 써보겠습니다.

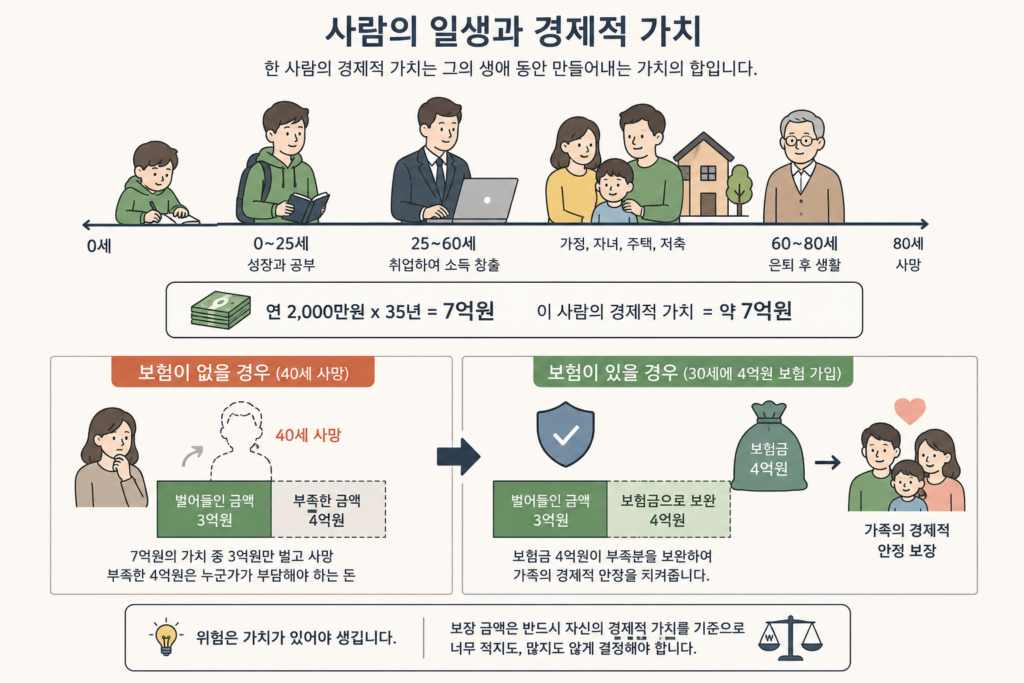

어떤 사람이 80세를 살다가 죽습니다.

태어나서 한 25년 공부하고 취직하여 60세까지 돈을 벌었습니다. 그 동안 결혼하여 가정도 꾸리고 자녀를 낳고, 집도 사고 저축도 해서 은퇴할 때 모아 둔 돈으로 80세까지 살다가 그렇게 죽었습니다.

매년 2,000만원의 돈을 벌었다고 하면 평생 번 금액은

2,000만원 x 35년 = 7억 원입니다.

결국 이 사람의 경제적 가치는 7억 원이라고 할 수 있겠군요. 25년 동안 성장하고 공부한 비용은 부모님이 부담했으니 실제로 그의 가치는 더 크겠지만 일단 논외로 하겠습니다.

이 사람은 자신의 가치 7억 원을 활용하여 가족의 생활비와 자녀의 교육비 등을 부담하고 저축한 돈으로 은퇴 후 생활비를 사용하고 다 쓰고 죽었습니다.

그런데 만약 이 분이 40세에 불의의 사고로 죽는다면 어떤 일이 벌어질까요? 7억 원의 가치가 있는 분이 3억 원 밖에 벌지 못했으니 모자란 4억은 누군가가 부담해야 하는 돈이 되었겠지요? 이 돈을 누가 부담해 줄까요?

그런데 이 분이 만약 30세쯤 4억 원의 보험에 가입했다면 어땠을까요? 실제로 이런 계산은 매월의 현금유입에 따른 할인 등 고려해야 할 사항이 많지만 대략 위험에 대한 측정은 이런 식으로 해야 한다는 이야기입니다.

위험은 가치가 있어야 생기는 것이고 사람보다 더 가치 있는 것은 없습니다. 보장하는 금액은 반드시 그의 경제적 가치를 기준으로 산정되어야 하며 그 가치보다 턱없이 적거나 많지 않게 결정되어야 합니다.

그런데 많은 분들이 사망에 대한 보장보다는 살아있을 때를 보장해 주는 보험을 선호하십니다. 그런데 여기에도 매우 큰 함정이 숨어 있습니다. (계속)

—————-

The Human Life Cycle and Economic Value

Coverage, in English, is called “Protection.” It literally means being protected. But protected from what? People often say we need protection from dying too early or living too long. Instead of repeating textbook definitions, let us approach the idea differently.

Suppose a person lives to the age of 80.

They spend about 25 years growing up and studying, then begin working and earn income until the age of 60. Along the way, they get married, raise children, buy a house, save money, and eventually retire. Using the assets accumulated during their working years, they continue living until age 80 and then pass away peacefully.

If this person earned 20 million KRW annually, the total lifetime income would be:

20 million KRW × 35 years = 700 million KRW

In other words, this individual’s economic value can be considered approximately 700 million KRW.

Of course, the actual value would be even greater if we included the cost borne by the parents during the first 25 years of growth and education, but let us set that aside for now.

This person used that economic value of 700 million KRW to support their family’s living expenses, pay for their children’s education, save money, and fund their retirement until the end of life.

But what if this person died unexpectedly at age 40?

A person with an economic value of 700 million KRW would have earned only about 300 million KRW by then. The remaining 400 million KRW would effectively become a financial burden someone else must absorb.

Who would bear that cost?

Now imagine that this person had purchased a 400 million KRW insurance policy around age 30. Although real-world calculations require more detailed considerations such as discounting future cash flows, this example illustrates the basic principle of how risk should be measured.

Risk only exists where value exists, and nothing is more valuable than human life. Therefore, the amount of coverage should always be determined based on a person’s economic value—not set excessively low or unrealistically high compared to that value.

However, many people prefer insurance products that provide benefits while they are alive rather than insurance covering death.

Yet even here, a very significant trap exists. (To be continued)