질병보험의 허와 실

암 보험에 가입한 분들에게 묻습니다.

왜 암 보험에 가입하셨나요?

열이면 열 모두 “암에 걸린 사람이 있는 집을 알고 있는 데 돈을 무척 많이 쓰고 가셔서 남은 가족들이 다들 경제적으로 고생하더군요. 우리 집은 그러지 않으려고 식구 별로 한 두 개씩은 가입하고 있습니다.” 라고 말씀하시곤 합니다.

그런데 말입니다.

암 보험에 대해서 잘 알고 계십니까?

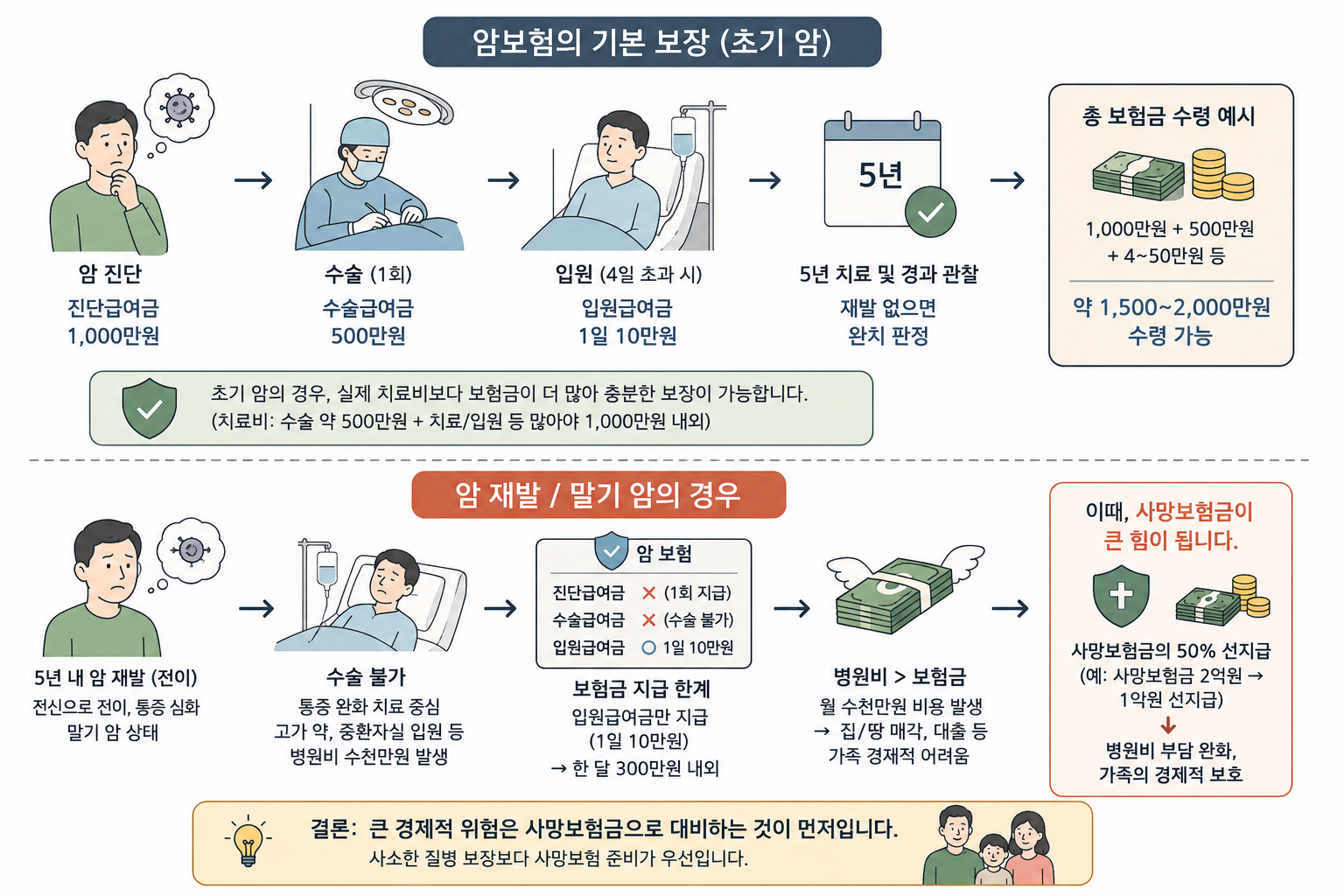

통상 암 보험은 기본적으로 암이라는 진단을 받으면 1,000만원의 진단자금을, 암으로 수술하면 수술할 때마다 회당 500만원, 암으로 입원하면 4일 초과시 1일당 10만원의 입원보험금을 지급하는 보험입니다.

이 보험에 가입한 분이 암에 걸렸다고 가정을 해 보지요. 처음 암이라고 진단을 받으면 진단급여금 1,000만원이 지급됩니다. 요즘은 진단 기술이 발달하여 보통 1~2기면 발견할 수 있다고 합니다. 그 후 병원에서는 수술 날짜를 정하고, 수술을 하고, 약 1주일 정도 입원한 뒤에 퇴원을 합니다. 그리곤 방사선 치료도 하고 약물치료도 하고, 하여튼 한 5년 간 꾸준히 치료하고 검사하며 경과를 살피게 됩니다. 만일 이 5년 동안 암이 재발하지 않으면 “완치” 판정을 합니다.

그런데 그 동안 들어간 비용을 계산해 보면 수술비용 약 500만원, 치료비용 및 병실료 등 많아야 1,000만원 정도일까요? 물론 요즘은 국민건강보험에서 많은 부분을 보조 받아 훨씬 적게 들어간답니다.

그런데 보험금은 얼마나 받을까요?

진단 시 진단자금 1,000만원, 수술 시 수술자금 500만원, 입원 시 입원급여금 4~50만원 등등 적어도 1,500~2,000만 원가량 받게 됩니다.

충분한 금액을 받았으니 충분한 보장이 된 것이지요?

그런데 반전이 숨어있습니다.

만일 5년 내에 암이 재발하게 되면 어떻게 될까요?

재발이란 말은 암이 다른 부위로 전이되었다는 이야기입니다. 즉, 암세포가 전신에 퍼졌을 가능성이 있다는 이야기가 되고, 통증이 무척 심해지며, 쉽게 이야기하는 말기 암이 되었다는 상태일 것입니다.

말기 암 환자를 치료하는 것 보셨습니까?

말기 암환자의 경우 특별한 경우가 아니면 거의 수술할 수 없습니다. 통증이 너무 심하기 때문에 주로 통증을 완화하는 데 중점을 둡니다. 건강보험에서 지정한 진통제 정도로는 듣지 않기 때문에 단위가 높은 비싼 수입 약을 써야 하며, 수시로 중환자실에 입원하여야 하고, 병원비가 수 천 만원 가까이 들게 됩니다.

그런데 이 경우에는 암 보험이 어떤 역할을 할까요?

진단 급여금은 1회만 지급하는 항목이므로 다시 지급되지 않습니다. 수술을 하지 않으니 수술급여금 역시 받을 수 없습니다. 오직 하루에 10만원 나오는 입원급여금으로 그 비용을 감당해야 하는 것이지요. 비용은 한 달에도 수 천 만원이 나오는 데 보험에서는 겨우 300만원이 지급되는 상황입니다. 아무리 좋은 암 보험을 가입했다 해도 감당하기 어렵습니다. 그래서 집 팔고 논 팔고 돈 빌리러 다니고, 결국 가족들의 생활이 매우 어려워지는 것이지요.

실은 이런 경우가 바로 사망보험금이 빛을 발하는 순간일 것입니다. 사망보험금의 50%가 지급되는 것이지요. 사망보험금이 2억 정도 된다면 우선 1억 원이 지급될 것이고, 이것으로 병원비를 부담해야 하는 상황입니다.

이제 아셨나요?

실제로 대부분의 큰 부담을 사망보험으로 보장할 수 있는데도 불구하고 보험에 대한 오해와 편견이 이를 가로막고 있다면 매우 큰 손실이 아닐 수 없습니다. 보험에 가입한다면 사소한 각종 질병에 대한 보장보다는 사망보험의 준비가 먼저입니다. (계속)

—————-

Illusions and Reality of Disease Insurance

To people who have purchased cancer insurance, here is a question:

Why did you buy cancer insurance?

Almost everyone gives a similar answer:

“I know a family that suffered financially because someone developed cancer and spent an enormous amount of money before passing away. I do not want my family to go through that, so each family member has one or two cancer insurance policies.”

But do you truly understand how cancer insurance works?

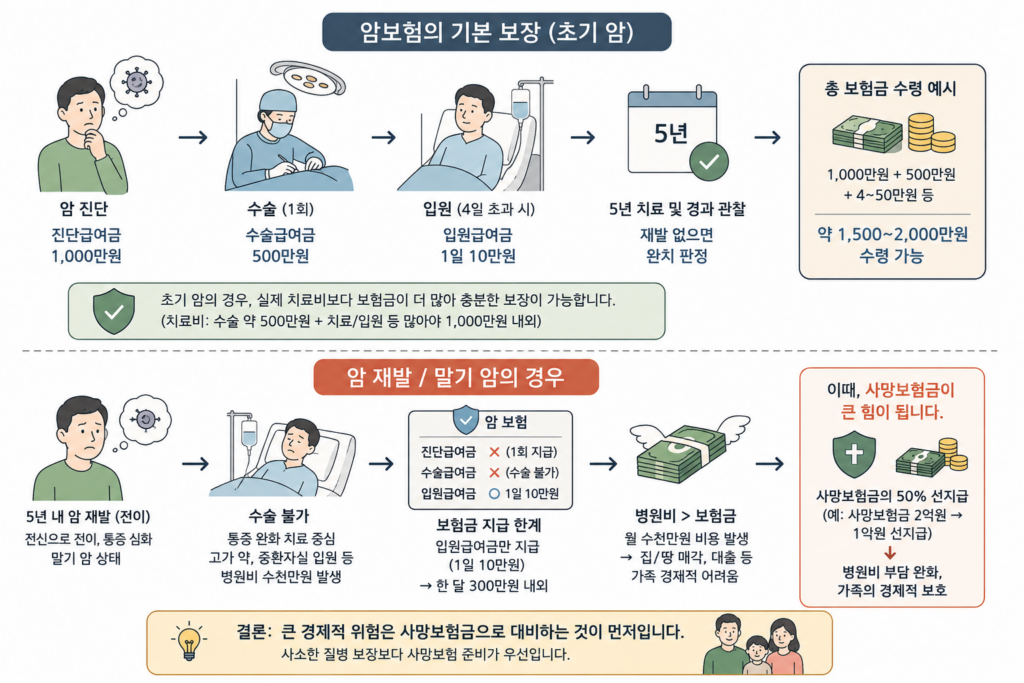

Typically, cancer insurance provides a diagnosis benefit of around 10 million KRW when cancer is diagnosed, a surgical benefit of approximately 5 million KRW per surgery related to cancer, and hospitalization benefits of around 100,000 KRW per day after the fourth day of hospitalization.

Now let us assume someone with this insurance develops cancer.

When the diagnosis is first confirmed, the insured receives the 10 million KRW diagnosis benefit. Nowadays, medical technology has advanced enough that cancer is often detected at stage 1 or 2.

The hospital then schedules surgery, performs the operation, and the patient is hospitalized for about a week before being discharged. Afterward, radiation therapy, medication treatment, and continuous monitoring continue for roughly five years. If there is no recurrence during that period, the patient is considered “fully cured.”

So how much does all of this actually cost?

Surgery may cost approximately 5 million KRW, and including treatment costs and hospitalization expenses, perhaps around 10 million KRW in total at most. In reality, because Korea’s National Health Insurance covers a substantial portion of treatment expenses, the actual out-of-pocket cost is often much lower.

Then how much does the insurance company pay?

Approximately 10 million KRW for diagnosis, 5 million KRW for surgery, and several hundred thousand KRW for hospitalization benefits—typically totaling around 15 to 20 million KRW.

That sounds like sufficient coverage, doesn’t it?

But there is a hidden reversal.

What happens if the cancer recurs within five years?

Recurrence means the cancer has metastasized to other parts of the body. In other words, cancer cells may have spread systemically, pain becomes extremely severe, and the condition effectively enters what people commonly call terminal cancer.

Have you ever seen the treatment process for terminal cancer patients?

In most terminal cancer cases, surgery is no longer possible. Treatment focuses primarily on pain management because the suffering becomes unbearable. Standard painkillers covered by health insurance are often ineffective, requiring expensive imported medications with stronger dosages. Patients frequently require intensive care unit hospitalization, and medical expenses can climb into tens of millions of KRW.

So what role does cancer insurance play in that situation?

The diagnosis benefit is paid only once, so no additional diagnosis benefit is provided. Since surgery is usually impossible, surgical benefits are not paid either. The patient must rely almost entirely on the hospitalization benefit of around 100,000 KRW per day.

While medical expenses may reach tens of millions of KRW per month, the insurance payout may amount to only around 3 million KRW monthly. Even with a relatively strong cancer insurance policy, covering such costs becomes extremely difficult.

That is why families end up selling homes, liquidating land, borrowing money, and ultimately suffering severe financial hardship.

In reality, this is precisely the moment when death benefit coverage demonstrates its true value.

At that stage, 50% of the death benefit may be paid in advance. If the policy includes a death benefit of 200 million KRW, then approximately 100 million KRW could be paid upfront, providing funds to cover the overwhelming medical expenses.

Do you understand now?

In practice, most catastrophic financial burdens can already be addressed through death benefit coverage. If misunderstandings and prejudice against insurance prevent people from preparing properly, the resulting financial loss can be enormous.

When purchasing insurance, preparing sufficient death benefit coverage should come before focusing on minor disease-related coverage. (To be continued)