Episode 40: 만기에 돌려받는 보험이 좋다고?

앞에서 보험료의 구성에 대해 잠깐 설명 드렸습니다만 모든 보험은 납입하는 보험료 중에서 보험회사가 경비로 쓰는 부가보험료와 보장을 위해 적립하는 위험보험료는 돌려받지 못하는 돈이라고 했습니다. 즉, 납입하면 소멸되는 항목이라는 이야기지요. 결국 저축보험료 만을 적립해서 만기에 돌려주는 것입니다.

소멸성 보험과 돌려주는 보험

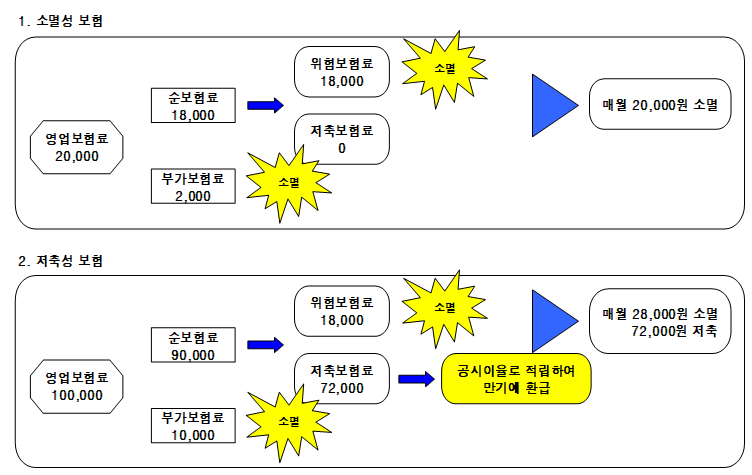

어떤 보험회사가 한 달에 2만원을 내면 1억 원을 보장해 주는 보험상품을 만들었습니다. 매월 2만원을 내고 버리는 상품이지요.

보험료를 뜯어보니 위험보험료가 18,000원이고, 부가보험료가 2,000원으로 구성되어 있습니다. 그런데, 잘 팔리지가 않습니다. 고객들이 소멸성 보험이라고 싫다고 한답니다.

보험회사는 할 수 없이 10만원의 보험을 다시 만듭니다. 보장의 내용은 2만 원짜리 보험과 똑 같아서 위험보험료는 18,000원이고, 저축성 보험료를 72,000원 추가하고 부가보험료는 10,000원을 받기로 했습니다. (통상 부가보험료는 순 보험료에 대한 일정한 비율로 책정합니다.) 이 보험은 만기에 납입한 보험료보다 더 많은 돈을 돌려주는 보험입니다. 그런데 이렇게 만들어 두니 잘 팔립니다.

이야기를 한 번 뜯어보지요.

소멸성 보험은 매월 2만원을 버리는 대신 1억 원을 보장받는 보험입니다. 돌려받는 보험은 매월 10만원 중 위험보험료 18,000원과 부가보험료 10,000원 해서 28,000원을 버리고 1억 원을 보장받는 상품입니다.

만기에 돌려받는 돈은 72,000원씩 시중금리에 연동된 실세금리로 저축하고 있는 것이지요. 이 돈이 아마 20년쯤 뒤에는 이자가 붙어서 납입 원금 이상으로 불어 있을 것입니다.

그런데 여러분이라면 같은 보장에 28,000원을 내겠습니까? 아니면 20,000원을 내겠습니까? 또 같은 저축이라면 72,000원을 저축하겠습니까? 아니면 80,000원을 저축하겠습니까?

보장도 되고 저축도 되는 보험상품은 그 만큼 비효율적이라는 것이지요. 그런데 우리의 보험에 대한 오해가 거꾸로 가입하게 만든다는 것을 인정하셔야 합니다. 보장을 받기 위해 가입하는 상품이라면 위험보험료와 부가보험료로만 구성된 보험이 최선이라는 것을 기억하십시오.

—————-

Episode 40: Is an Insurance Policy That Returns Money at Maturity Really Better?

Earlier, the structure of insurance premiums was briefly explained. In every insurance policy, part of the premium consists of the loading premium used by the insurance company for operational expenses and the risk premium reserved for coverage. These portions are not refundable. In other words, once paid, they are extinguished costs.

Ultimately, only the savings premium is accumulated and returned at maturity.

Term Insurance vs Refundable Insurance

Suppose an insurance company creates a product that provides coverage of 100 million KRW for a monthly premium of 20,000 KRW.

This is a pure protection-type insurance product where the monthly premium is essentially consumed in exchange for coverage.

Breaking down the premium structure, 18,000 KRW is allocated to the risk premium, while 2,000 KRW is allocated to the loading premium.

However, the product does not sell well because customers dislike the idea of “consumable insurance” where no money is returned at maturity.

As a result, the insurance company creates another product costing 100,000 KRW per month.

The coverage itself is exactly the same as the 20,000 KRW policy, meaning the risk premium remains 18,000 KRW. However, an additional 72,000 KRW is added as a savings premium, and the loading premium increases to 10,000 KRW. (Typically, loading premiums are calculated as a percentage of the net premium.)

This new product promises to return more money than the total premiums paid by maturity.

And surprisingly, this product sells very well.

Now let us analyze the situation carefully.

The consumable insurance policy provides 100 million KRW of coverage while costing only 20,000 KRW per month.

The refundable insurance policy provides the exact same 100 million KRW coverage, but out of the 100,000 KRW monthly premium, 18,000 KRW goes to the risk premium and 10,000 KRW goes to the loading premium. In other words, 28,000 KRW is effectively consumed every month for the same level of protection.

The remaining 72,000 KRW is simply being saved at a market-linked interest rate. After about 20 years, interest accumulates and the amount may grow beyond the original principal paid.

But if you had to choose, would you rather pay 28,000 KRW or 20,000 KRW for the exact same insurance coverage?

And if you were saving money anyway, would you rather save 72,000 KRW or 80,000 KRW?

Insurance products that attempt to combine protection and savings inevitably become less efficient in both areas.

Yet misconceptions about insurance often lead consumers to choose the opposite.

If the purpose of insurance is protection, then the most efficient product is one composed only of risk premiums and loading premiums.