Episode 42 : 가입한 보험을 해약하는 것은 무조건 손해라고?

일반적으로 보험에 가입했다가 해약하는 것은 손해가 분명합니다. 미리 쓴 부가보험료(신계약비)를 모두 내야 하기 때문에 해지환급금이 납입한 금액 대비 적을 가능성이 크기 때문입니다. 그런데 다른 관점으로도 한 번 생각해 볼 필요가 있습니다.

보장성 보험의 경우

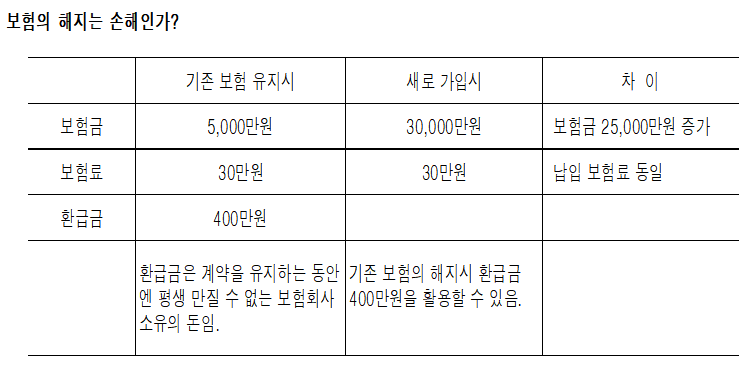

경제적 가치가 3억 원인 어떤 사람이 보장성 보험인 종신보험에 가입하고 있습니다. 한 달에 25만원을 보험료로 내고 있고, 5,000만원의 주계약보험금(사망보험금)에 각종 특약(질병특약 등)이 부가되어 있고 납입기간이 짧게 설정되어 있어 생각보다 많은 보험료를 납입하고 있습니다.

그런데 이 사람에게 필요한 보장금액은 3억 원이므로 2억5천만 원의 보험을 더 가입해야 하는 데. 기존의 보험을 유지하며 증액을 하려니 25만원을 추가하여 총 55만원의 보험료를 납입해야 한답니다. 대부분 이런 상황이면 증액을 포기하게 되겠지요.

그런데 아예 새로 가입하며 납입기간을 길게 하면 30만원으로 3억 원을 준비할 수 있답니다.

이럴 경우 기존의 5,000만원을 보장하는 보험을 해약하고 같은 돈으로 3억 원을 보장하는 보험에 새로 가입하는 것이 이득일까요? 아니면 그냥 기존의 보험을 유지하는 것이 이득일까요?

해지환급금을 생각하면 당연히 기존 보험을 유지하는 것이 이득이겠습니다. 그런데 위험관리라는 측면에서 보면 이 분은 빵점 짜리 입니다. 필요한 보험금은 3억 원인데 5천 만원 만을 보장받고 계시니까요. 그러면서도 보험료는 동일하게 30만원을 내고 계신 거지요. 해지환급금에서 볼 손해 때문에 2억5천 만원의 위험을 안고 있는 상태입니다.

여기서 우리는 매우 큰 착각을 하고 있습니다.

그것은 해지환급금이 바로 내 돈이라고 하는 착각입니다.

종신보험은 100% 보장성 보험이라고 했습니다. 앞에서 보장을 받는 동안에는 보장받을 돈(보험금)이 고객의 돈이며, 보장의 기간이 끝나면 해지환급금이 고객의 돈이라고 설명 드렸지요?

종신보험의 보험기간은 평생입니다. 그렇다면 이 보험을 평생 유지하며 받을 돈은 사망보험금이지, 해지환급금이 아니라는 이야기입니다.

보험회사는 고객이 평균수명까지 살다가 죽는 경우를 가정하여 보험료를 책정하는 데 그 시점에서의 해지환급금이 사망보험금과 비슷해지도록 보험료를 결정한다고 했습니다.

즉, 고객이 예상보다 빨리 사망한다면 보험회사는 아직 해지환급금으로 보험금을 다 만들어 두지 못했기 때문에 손해를 보게 되지만, 다른 분들이 납입한 보험료로 부족분을 채우게 되고, 늦게 사망한다면 이미 납입한 보험료로 보험금 이상을 만들어 둘 수 있게 되어 보험금을 지급하고도 조금 돈이 남게 되는 것입니다.

즉, 보장을 유지하는 동안은 해지환급금은 고객이 평생 만질 수 없는 돈이라는 것이지요. 해지환급금을 받으려면 고객은 보험을 해지하고 보험금을 수령할 권리를 버려야 합니다. 그렇다면 기존의 불충분한 보험을 충분한 보험으로 바꾸는 행위는 제대로 된 위험관리를 시작하면서 평생 받을 수 없던 해지환급금을 돌려받는 것과 같습니다.

이 경우라면 기존 보험의 해지는 분명 이익인 것입니다. 우리가 손해라고 말하는 것은 준비 없이 보험을 해지할 때의 상황으로 보험도 버리고 원금도 손해 보는 상황일 경우이며, 보장도 못 받고 저축도 안 되는 경우입니다.

————-

Episode 42: Is Canceling an Insurance Policy Always a Loss?

In general, canceling an insurance policy after enrollment is indeed financially disadvantageous. Since the insurer has already used the upfront loading premiums (initial acquisition costs), the surrender value is often significantly lower than the total premiums paid.

However, the issue should also be viewed from another perspective.

In the Case of Protection-Type Insurance

Suppose a person with an economic value of 300 million KRW owns a whole life insurance policy, which is a protection-type insurance product. The individual pays 250,000 KRW per month in premiums. The policy includes a primary death benefit of 50 million KRW along with various riders such as disease-related coverage. Because the premium payment period is relatively short, the monthly premium burden is higher than expected.

However, this person actually requires coverage of 300 million KRW, meaning an additional 250 million KRW of coverage is still necessary.

If the person attempts to maintain the existing policy while adding more coverage, an additional 250,000 KRW per month would be required, resulting in total premiums of 550,000 KRW per month. In most cases, people in this situation give up on increasing coverage altogether.

But what if the person cancels the existing policy and instead purchases a new policy with a longer payment period? In that case, 300 million KRW of coverage may be obtainable for only 300,000 KRW per month.

So which choice is actually more beneficial?

Is it better to keep the original policy that covers only 50 million KRW, or to cancel it and purchase a new policy providing 300 million KRW of coverage for roughly the same monthly premium?

From the perspective of surrender value, maintaining the existing policy appears advantageous.

However, from the perspective of risk management, this person has completely failed.

The required coverage amount is 300 million KRW, yet only 50 million KRW is insured, while still paying 300,000 KRW per month. Due to fear of losing surrender value, the person remains exposed to an uninsured risk gap of 250 million KRW.

This reveals one of the biggest misconceptions people have.

Many assume that surrender value is automatically “their money.”

But whole life insurance is fundamentally a 100% protection-type insurance product.

Earlier, it was explained that during the coverage period, the money belonging to the policyholder is the insurance benefit itself, whereas after the coverage period ends, the surrender value becomes the customer’s money.

However, the coverage period of whole life insurance lasts for an entire lifetime.

That means the money the customer is actually intended to receive is the death benefit—not the surrender value.

Insurance companies calculate premiums based on the assumption that policyholders will live until average life expectancy. Premiums are structured so that by that time, the surrender value gradually approaches the death benefit amount.

If the insured dies earlier than expected, the insurance company has not yet accumulated enough surrender value to fully fund the death benefit, resulting in a loss that is compensated using premiums paid by other policyholders.

Conversely, if the insured lives longer than expected, the insurer may accumulate more than enough funds to pay the death benefit and still retain a surplus afterward.

In other words, while coverage remains active, the surrender value is effectively money the policyholder can never truly use during life.

To receive the surrender value, the customer must cancel the insurance policy and surrender the right to receive the insurance benefit itself.

Therefore, replacing inadequate insurance coverage with sufficient coverage is essentially equivalent to beginning proper risk management while recovering surrender value that would otherwise never have been accessible during life.

In such cases, canceling the old policy is clearly beneficial.

What people usually describe as a “loss” occurs when insurance is canceled without preparation—resulting in both the loss of coverage and financial loss on the principal. In other words, a situation where neither protection nor savings functions properly anymore.