효과적인 위험 관리 계획

위험에 대해 충분히 이해하셨습니까?

가치가 있는 곳에 위험이 발생하고, 이런 위험을 회피하기 위해 보험을 가입한다는 것을 충분히 이해해야만 효과적인 위험관리가 가능합니다. 보험회사는 장기적으로 거래해야 하는 곳이고, 가치에 대한 보장에 특화되어 있는 곳이므로 부가보험료의 구조를 잘 알아두면 매우 큰 이익을 얻을 수 있습니다.

우선 보험을 잘 활용하기 위해 몇 가지 알아두어야 하는 것이 있습니다.

우선 필요 없는 보험은 과감히 정리하라.

한정된 수입을 효율적으로 활용해야 하는 상황에서 내게 필요 없는 보험은 두 가지 측면에서 매우 큰 문제를 발생시킵니다.

첫째는 필요한 보장을 가질 수 없게 만드는 것이고,

둘째는 현금의 유동성을 떨어뜨리는 것입니다.

따라서 필요한 보험인 지 아닌 지 현명하게 판단하여 필요 없는 보험은 과감히 버려야 같은 비용으로 내게 필요한 보험을 준비할 수 있습니다. 보험은 친분에 의해 들어주는 것이 아닌 나의 필요에 의해서 가입하는 상품입니다. 하지만 이것을 판단하는 것은 매우 어려우므로 전문 상담사의 도움이 꼭 필요합니다.

효율적인 위험관리를 위한 보험의 가입 기준은 다음과 같습니다.

충분한 보험금을 설정하라.

5억 원의 가치가 있는 것은 5억 원의 보장을 받아야 하고, 10억 원의 가치가 있는 것은 10억 원의 보장을 받아야 합니다. 어떤 경우에도 충분하게 가치를 보장하지 못한다면 보험으로서의 의미가 없는 것이지요.

보장의 기간과 보험료의 납입은 길수록 좋다.

보험은 살아가는 과정에서 발생할 지도 모르는 위험에 대비하는 상품입니다. 위험은 언제 어떤 모습으로 다가올 지 모르므로 평생 동안 죽을 때까지 대비해 두어야 할 것입니다. 따라서 보장의 기간은 길수록 좋습니다. 보험의 가장 기본형이 종신보험인 이유가 바로 그것입니다. 그런데 이렇게 긴 보장을 받으며 보험료를 짧게 납입한다면 이 역시 보험의 관점에서 매우 큰 손해를 볼 수도 있습니다. 따라서 보험료의 납입기간도 긴 것이 좋습니다.

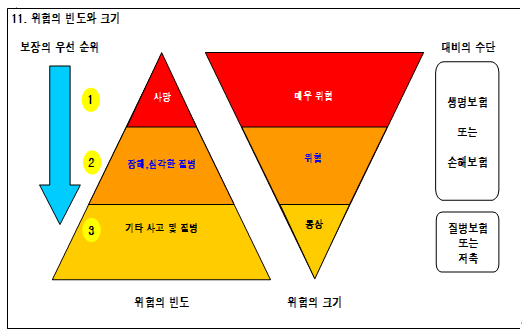

보장의 순서는 가치가 큰 것에서 적은 것으로 해야 한다.

위험의 확률과 가치의 크기는 반비례합니다. 사망의 확률은 낮은 반면 사망시의 가치 손실은 매우 크고, 질병의 확률은 매우 높은 반면 이로 인한 손실은 그리 크지 않습니다. 그렇다면 손실의 크기가 큰 것부터 작은 것으로 보장의 우선순위를 결정하는 것이 효율적입니다. 어린 자녀의 질병에 대한 보장보다는 돈을 벌어 오는 가장의 사망보장이 훨씬 중요합니다.

가급적이면 모든 범위를 보장받는 것이 좋겠지만 보험으로 모든 위험을 해결할 수는 없으며 또한 효율적이지 않습니다. 위험의 크기가 크지 않다면 보험이 아닌 저축으로 해결하는 것이 효율적입니다.

적정한 보험료를 납입한다.

보험료는 월수입의 10%이내가 적당하다고 합니다. 이 비용으로 필요한 보장을 100% 준비할 수 있어야 합니다.

위험관리는 계획이다.

보험은 한 번의 가입으로 끝나는 상품이 아니라 평생에 걸쳐 조정하고 수정해야 하는 계획입니다. 삶의 상황에 따라 보험금을 조절하며 유지해 가야 하는 상품이란 것입니다. 이렇게 중간중간 조정하며 손해 보지 않으려면 처음부터 그 기본을 잘 만들어 두어야 합니다.

그 기본이 바로 긴 납입기간의 설정입니다. 긴 납입기간은 유지하는 중간에 줄일 수도 있지만, 짧은 납입기간을 늘릴 수는 없습니다. 우선은 길게 설정해 두고, 수시로 전문가와 상의하여 수정해야 한다는 것을 기억하십시오.

다시 한 번 정리하자면 은행은 대출 거래에 최적인 금융기관이고, 증권회사는 중단기 투자가 최적인 금융기관이며, 보험회사는 보장에 최적인 금융기관입니다. 이것을 적절하게 취사선택 하는 것이 바로 금융거래의 백전불태 전략입니다.

—————-

Effective Risk Management Planning

Have you fully understood the nature of risk?

Risk arises wherever value exists, and effective risk management becomes possible only when people clearly understand that insurance exists to help avoid or transfer those risks. Insurance companies are institutions designed for long-term financial relationships and are highly specialized in protecting economic value. Therefore, understanding the structure of insurance expenses and loading premiums can provide significant long-term financial advantages.

First, there are several important principles that must be understood in order to utilize insurance effectively.

First, eliminate unnecessary insurance without hesitation.

When income is limited and financial resources must be used efficiently, unnecessary insurance creates two major problems.

First, it prevents you from securing the coverage you actually need.

Second, it reduces cash flow liquidity.

Therefore, policies should be evaluated carefully and unnecessary insurance should be eliminated decisively so that truly necessary coverage can be secured at the same overall cost. Insurance should never be purchased merely because of personal relationships or social pressure. Insurance must be purchased according to genuine personal needs.

However, making such judgments correctly is extremely difficult, which is why professional consultation is essential.

The standards for effective risk management through insurance are as follows.

Set Sufficient Coverage Amounts

An individual with an economic value of 500 million KRW should receive 500 million KRW in coverage, while someone with a value of 1 billion KRW should receive 1 billion KRW in protection.

If insurance fails to provide sufficient protection for actual economic value, then it fundamentally loses its purpose as insurance.

Longer Coverage Periods and Longer Premium Payment Periods Are Better

Insurance exists to prepare for risks that may arise throughout life.

Because risks can appear unexpectedly and in any form, protection should ideally continue for an entire lifetime. That is why the longer the coverage period, the better.

This is precisely why whole life insurance represents the most fundamental form of insurance.

However, receiving lifelong protection while paying premiums over a short period can create substantial financial inefficiency from an insurance perspective.

Therefore, longer premium payment periods are generally preferable as well.

Protection Priorities Should Follow Economic Value

The probability of risk and the size of potential financial loss are inversely related.

The probability of death is relatively low, but the financial loss caused by death is extremely large.

Conversely, illnesses occur far more frequently, but the financial losses they create are generally smaller.

Therefore, insurance priorities should begin with the risks associated with the largest potential losses and then move toward smaller risks.

For example, the death protection of a primary income earner is far more important than insurance coverage for minor illnesses affecting young children.

Ideally, all risks would be fully insured. However, insurance cannot solve every type of risk, nor would doing so be efficient.

If the size of a potential loss is relatively small, it is often more efficient to prepare through savings rather than insurance.

Pay Appropriate Premium Amounts

Insurance premiums are generally considered appropriate when they remain within 10% of monthly income.

Within that budget, essential coverage should be prepared as completely as possible.

Risk Management Is a Lifelong Plan

Insurance is not a product that ends after enrollment.

It is a lifelong plan that must be continuously adjusted and revised over time.

Coverage amounts should be modified according to changes in life circumstances and economic conditions.

To make these adjustments efficiently without unnecessary financial losses, the initial structure of the insurance plan must be designed properly from the beginning.

The core foundation is establishing a long premium payment period.

A long payment period can later be shortened if necessary, but a short payment period cannot easily be extended afterward.

Therefore, it is best to establish long-term structures initially and continue revising them regularly through consultation with financial professionals.

To summarize once again:

Banks are financial institutions optimized for lending transactions.

Securities companies are optimized for short- and mid-term investments.

Insurance companies are optimized for protection and risk management.

Selecting and utilizing each financial institution appropriately according to its strengths is the true “invincible strategy” of financial management.