우선 연금보험은 장기 상품입니다.

위의 상품이 백만 원 씩 10년을 납입하고 20년을 예치해 둔 상태에서 삼십 년 후에 연금으로 전환하는 상품이든, 30년을 납입하고 바로 연금으로 전환하는 상품이든 간에 분명한 것은 연금으로 전환하는 시점에 모여 진 해지환급금을 기준으로 연금을 지급한다는 것입니다.

이 연금은 평생 받는 돈이고 연금으로 전환한 이후에는 해지가 되지 않기 때문에 실제로 서른 살에 평생 거래할 상품에 가입한다는 의미입니다.

그러니 가입하는 시점에 매우 많은 부분을 고려해야 하지 않을까요?

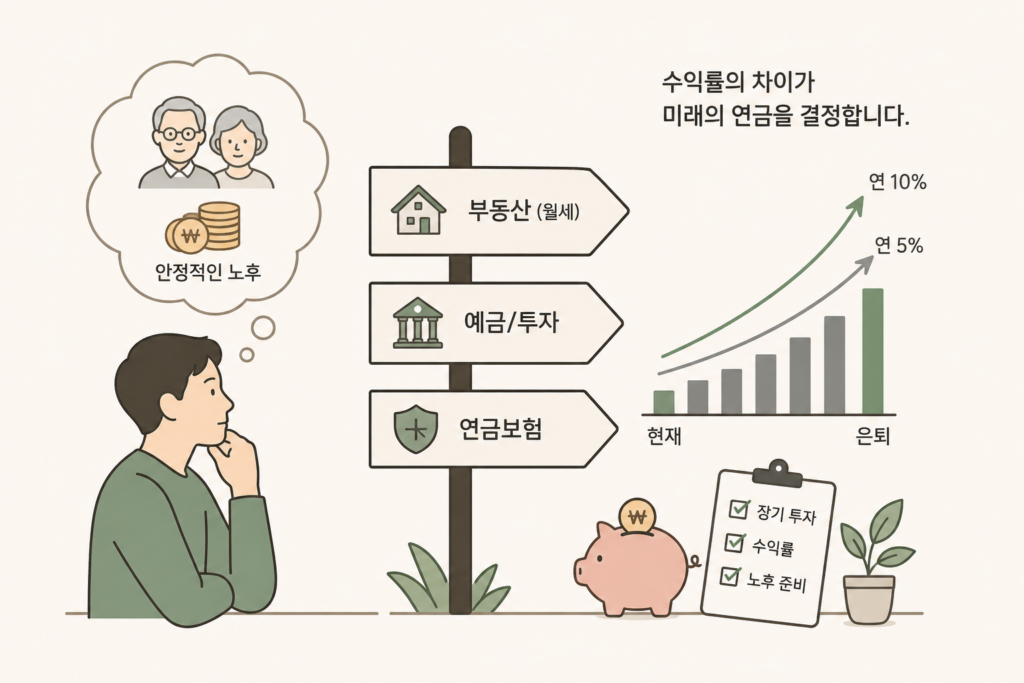

첫 번째 고려할 것은 바로 수익률에 대한 것입니다.

연금보험의 수익률이 과연 얼마나 될까요? 연금보험을 바라보는 관점은 바로 안정성입니다. 안정성이라는 이야기는 수익성이나 유동성에서는 손해를 보겠다는 이야기지요.

대부분의 연금보험이 4~5%의 수익률을 제시합니다. 물론 이것은 시중의 실세금리를 이야기 하는 것이고, 나중에는 더 떨어질 수도 있겠지요. 수익을 조금 더 키울 수 있도록 변액연금이라는 상품도 판매되고 있지만 이 역시 안정성에 기준을 두고 있어서 채권의 편입비율이 높은 펀드에 투자하고 있고, 따라서 수익률은 그리 높지 않은 편입니다.

아직 젊은 분이 연금보험에 가입하는 상황이라면 앞에서 살펴 본 가격변동성이 큰 상품에 장기투자 하는 방법이 수익을 극대화하는 방법이란 것을 기억하기 바랍니다.

통상 일반 연금보험 보다 수익이 높을 것으로 예상되는 변액연금보험도 연금보험이란 이름 아래 수익의 안정성을 내세워 수익률 측면에서 많은 희생을 하고 있는 상품입니다.

장기 상품에 그리 필요하지 않아 보이는 원금보존을 위해 원금보존 비용을 납입하고 있고, 장기투자임에도 불구하고 가격의 변동성이 큰 주식형이 아닌 안정적인 (수익이 낮은) 수익률의 채권에 많은 부분을 투자하고 있고, 하여튼 장기 상품에 걸맞지 않은 이름의 비용들이 여기저기 붙어 있는 상품이란 말이지요. 이렇게 낮은 수익률의 상품으로 30년을 거래한다면 나중에 적립된 해지환급금은 매우 적은 수준일 것입니다.

만일 같은 돈을 채권형인 변액연금이 아닌 주식형인 변액유니버셜보험에 납입한다면 어떨까요? 둘 다 장기 투자상품이므로 원금보존이란 것은 큰 의미가 없을 것입니다. 주식형 펀드의 수익률을 연 10%로 가정하고, 채권형 펀드의 수익률을 약 5%로 가정한다면 채권에 60%, 주식에 40%를 편입한 변액연금 펀드의 수익률은 연 7% 정도입니다.

그러나 주식에 100%를 편입한 변액유니버셜보험 펀드의 수익률은 연 10%가 되겠지요? 만일 연 3%의 수익률 차이가 30년간 지속된다면 산술적으로도 근 90% 이상의 수익률 차가 될 것입니다. 물론 위의 예는 극단적인 예이지만 문제는 연금전환을 요청하는 시점에서 3억 원의 환급금이 있는 것과 4억 원의 환급금이 있는 것은 매우 큰 차이라는 것입니다.

연금을 받기 위해 연금보험에 가입해야 한다는 고정관념을 버려야 돈을 조금 더 효율적으로 활용할 수 있을 것입니다. 노후에 많은 연금을 받고 싶다면 젊어서 많은 돈을 연금보험에 가입하지 마십시오.

만일 대부분의 저축을 연금보험에 하고 있다면 평생 충분한 돈을 만져보기 힘들 것입니다. 은퇴할 때까지는 효율적인 저축과 투자를 통해 은퇴에 충분한 금액을 마련하고, 은퇴 시점의 상황에 따라 일시납 연금보험에 가입하든, 부동산을 구입하든, 목돈으로 넣어두고 필요한 만큼 인출하여 쓰든 하는 것이 가장 효율적인 방법이라는 것입니다..

노후에 좀 더 많은 연금이 필요하다면 지금부터라도 변동성이 매우 큰 펀드에 꾸준히 장기적으로 투자하십시오. 그리고 혹시라도 가격이 떨어진다면 조금 더 투자하시고 가격이 오른다면 조금 덜 투자하십시오. 일반 금융소비자가 충분한 수익을 낼 수 있는 방법은 투자의 원칙에 충실하게 따르는 것 밖에 없습니다.

———————

The Illusion and Reality of Annuity Insurance

First, annuity insurance is fundamentally a long-term financial product.

Whether the product involves paying premiums of one million KRW per month for ten years and leaving the funds invested for another twenty years before converting them into annuity payments thirty years later, or paying premiums continuously for thirty years before immediately beginning annuity payments, one fact remains the same:

The annuity payments are ultimately calculated based on the surrender value accumulated at the moment the policy is converted into an annuity.

Because annuity payments continue for life and the contract generally cannot be canceled after annuitization, purchasing annuity insurance at age thirty effectively means entering into a lifelong financial relationship with the product.

Therefore, should people not consider a tremendous number of factors before enrolling?

The first consideration is investment return.

What kind of return can annuity insurance realistically generate?

The fundamental characteristic of annuity insurance is stability.

But emphasizing stability inherently means sacrificing profitability and liquidity.

Most annuity insurance products offer returns of approximately 4–5%, generally linked to prevailing market interest rates. Of course, those rates may decline even further in the future.

Insurance companies also sell products called variable annuities in an attempt to improve returns somewhat. However, even those products prioritize stability, which means they invest heavily in bond-oriented funds. As a result, their returns also tend to remain relatively modest.

If a person is still young when considering annuity insurance, they should remember the principle discussed earlier: long-term investment in highly volatile growth assets is often the most effective way to maximize returns.

Even variable annuity insurance, which is generally expected to outperform traditional annuity insurance, still sacrifices considerable return potential in the name of stability simply because it carries the label “annuity.”

These products incur costs for principal protection that may not even be necessary for truly long-term investments.

Despite being long-term products, they allocate large portions of assets into stable but lower-return bond investments instead of higher-volatility equity investments that historically generate stronger long-term growth.

In short, annuity insurance products often contain numerous expenses and structural limitations that appear poorly suited for genuine long-term investing.

If someone remains invested in low-return products like these for thirty years, the accumulated surrender value at retirement may ultimately be far smaller than expected.

Now consider a different scenario.

What if the same money were invested not into a bond-oriented variable annuity, but instead into an equity-focused variable universal life insurance product?

Both are long-term investment vehicles, meaning short-term principal preservation should not matter significantly.

Suppose stock-oriented funds generate annual returns of 10%, while bond-oriented funds generate annual returns of 5%.

A variable annuity fund invested 60% in bonds and 40% in equities would produce an approximate annual return of 7%.

Meanwhile, a variable universal life insurance fund invested 100% in equities could generate returns closer to 10%.

If that 3% annual return difference continues for thirty years, the mathematical difference in final accumulated assets could exceed 90%.

Of course, this example is intentionally extreme.

However, the truly important point is this:

At the moment annuity conversion begins, there is a massive difference between having accumulated 300 million KRW and having accumulated 400 million KRW.

People must abandon the fixed idea that annuity income requires purchasing annuity insurance.

Only then can financial resources be utilized more efficiently.

If someone wants to receive larger annuity income during retirement, then while still young, they should avoid placing excessive amounts of money into traditional annuity insurance products.

If the majority of one’s savings remain locked into annuity insurance for an entire lifetime, it may become difficult to access and utilize meaningful amounts of wealth throughout life.

A far more efficient strategy is to build sufficient retirement assets through efficient saving and investing during working years, then decide at retirement whether to purchase a lump-sum immediate annuity, invest in real estate, or simply place assets into financial instruments and withdraw funds as needed.

If greater retirement income is truly desired, then beginning now, individuals should consistently invest long-term into highly volatile growth-oriented funds.

And if prices decline, invest a little more.

If prices rise sharply, invest a little less.

For ordinary financial consumers, the only reliable way to achieve meaningful long-term returns is to follow the fundamental principles of investing with consistency and discipline.