저축성 보험의 경우

저축성 보험의 경우 보장의 목적보다는 저축의 목적으로 가입하는 상품입니다. 그런데 저축보험료를 적립해 두는 방법에 몇 가지 알아두어야 할 것이 있습니다.

저축보험료를 적립하는 방법은 크게

예정이율(고정된 이자율)에 따라 적립하는 방법

공시이율(변동되는 이자율)에 따라 적립하는 방법

수익률에 따라 적립하는 방법이 있습니다.

예정이율은 고정금리를 적용하여 이자를 지급하는 방법입니다. IMF 이전의 대부분 상품이 예정이율을 적용하여 이자를 지급했고, 회사가 예정이율보다 높은 이자수익을 얻게 되면 이익부분을 배당하기도 하였습니다. 물론 손실이 발생하더라도 예정된 이자는 지급해야 하는 것이지요.

IMF이후에는 대부분 공시이율을 적용합니다. 이것은 시중의 실세금리를 적용하여 이자를 지급하므로 회사가 이익이나 손해로부터 비교적 자유롭게 되지요.

수익률을 적용하는 것은 변액보험(Variable Insurance)의 경우입니다. 저축보험료를 보험회사가 아닌 외부의 기관에서 펀드에 투자하기 때문에 회사는 투자 수익으로부터 완전히 자유롭게 경영을 하게 됩니다.

이런 흐름으로 저축보험료의 관리방법이 변화하게 된 이유는 바로 IMF로 인해 초래된 시장개방과 저금리 때문입니다. 시중금리가 인하되며 보험회사는 자신의 책임 하에 고정금리로 운용하던 저축보험료의 수익을 보장할 수 없을 것으로 판단하여 이를 공시이율로 변경했는 데 이 또한 너무 낮은 금리로 고객의 수익을 충분히 확보할 수 없을 것으로 판단하여 수익률이 높은 펀드 투자로 전환하게 된 것이지요.

처음에는 회사의 경영부담을 완화하기 위한 조치이고, 두 번째는 고객의 수익을 확보하기 위한 조치라고 볼 수 있습니다.

문제는 잘 알지 못하고 저축성 보험에 가입한 고객의 상황에서 어떤 판단을 해야 하는가 입니다.

저축성 보험도 역시 장기저축계획의 일환이므로 적당한 금액을 효율적으로 납입하는 것이 원칙입니다. 즉, 장기간 납입하여야 하는 상품이므로 부담스러운 금액을 납입한다면 오래 지속하기 어렵습니다.

수입 중에서 저축할 수 있는 금액 중 일부분만 장기상품에 납입하는 것이 오랫동안 유지하며 최대한의 이익을 취할 수 있다는 말입니다.

그런데 많은 분들이 가입 당시의 상황만을 반영하여 나중 일을 생각하지 않고 부담스러운 금액을 보험으로 가입합니다. 그리고는 갑작스런 상황 변화로 납입을 부담스러워 하곤 하지요. 그래서 해지를 하러 갔더니 반 밖에 안 돌려준답니다. 문제는 이 상황에서 대부분의 고객들은 둘 중의 하나로 결정하는 것 같습니다.

하나는 조금 부담스럽지만 원금을 회복할 때까지 기다리겠다는 결정이고, 또 하나는 당장 어려우므로 손해를 보더라도 해지를 하겠다는 결정입니다.

물론 둘 다 화가 나는 상황이지요. 여유가 있다면 첫 번째의 상황을 선택하는 분들이 대부분일 것입니다. 하지만 이것이 과연 옳은 결정일까요?

다시 한 번 생각해 보면 이렇습니다.

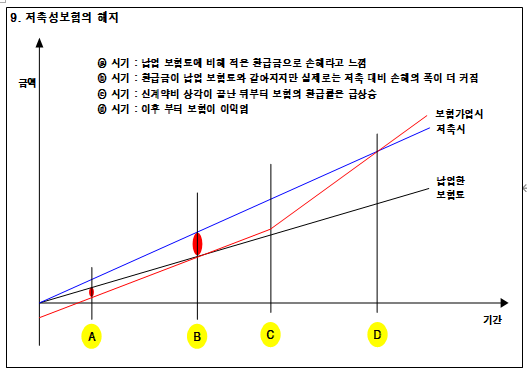

보험의 해지환급금이 적은 이유는 납입한 돈 중에서 부가보험료와 위험보험료를 제외하고 나머지만 돌려주기 때문이라고 말씀드렸지요? 게다가 일부 부가보험료를 선상각 하기 때문에 발생한 회복하지 못하는 손해도 포함되어 더욱 적은 금액을 돌려받는 것이지요. 그런데 시간이 지나면서 저축보험료에 대한 이자가 지속적으로 붙어 원금을 만드는 것처럼 보일 뿐이라는 것입니다. 즉, 원금에 도달하는 기간까지의 부가보험료와 위험보험료의 소멸부분은 절대 회복되지 않는다는 것이지요.

저축이라고 생각한다면 이 보다 바보 같은 짓이 없습니다. 차라리 지금 해지환급금을 받아 은행에 넣어두고 매월 보험료만큼을 적립한다면 훨씬 더 빨리 원금을 회복할 수 있을 것이니 말입니다. 적어도 계속 소멸되는 위험보험료와 일부 부가보험료의 손실은 줄일 수 있지 않습니까?

분명히 말씀드린다면 그 동안 납입한 보험료를 기준으로 보험의 해지는 반드시 손해입니다. 그러나 제대로 된 위험관리계획을 준비하기 위해 해지하는 것과 제대로 된 저축계획을 만들기 위해 해지하는 것은 분명히 고객에게는 이익입니다.

—————

In the Case of Savings-Type Insurance

Savings-type insurance products are primarily purchased for savings purposes rather than for protection. However, there are several important concepts people should understand regarding how savings premiums are accumulated.

Broadly speaking, savings premiums are accumulated through three methods:

- Accumulation based on an assumed interest rate (fixed interest rate)

- Accumulation based on a declared interest rate (variable interest rate)

- Accumulation based on investment returns

The assumed interest rate method applies a fixed rate of interest. Before the IMF financial crisis, most insurance products used assumed interest rates to determine returns. If the insurer generated returns higher than the assumed rate, the excess profit was sometimes distributed as dividends. Of course, even if losses occurred, the insurer was still obligated to provide the promised interest rate.

After the IMF crisis, most products shifted to declared interest rates. Under this system, interest is determined according to prevailing market rates, allowing insurance companies to become relatively free from profit and loss risks associated with fixed-rate guarantees.

The third method, accumulation based on investment returns, applies to variable insurance products. In these products, the savings premiums are invested into external funds rather than being directly managed by the insurance company, allowing insurers to operate independently from investment performance risks.

The reason these changes in savings premium management occurred was largely due to market liberalization and low interest rates following the IMF crisis.

As market interest rates declined, insurers concluded that they could no longer sustainably guarantee fixed returns through products using assumed interest rates. As a result, they shifted to declared interest rates. However, because even market-linked rates became too low to provide satisfactory returns to customers, insurers eventually introduced fund-based investment products with potentially higher returns.

The first change can therefore be viewed as a measure to reduce insurers’ financial burden, while the second aimed to improve customers’ investment returns.

The real issue, however, is what consumers should do when they purchased savings-type insurance products without fully understanding these structures.

Savings-type insurance should also be approached as part of a long-term savings strategy. The fundamental principle is to contribute manageable amounts efficiently over a long period.

Since these are products designed for long-term contributions, paying excessive premiums makes long-term maintenance difficult.

Only a portion of one’s available savings capacity should be allocated to long-term insurance products. That is the most effective way to maintain the product for an extended period while maximizing long-term benefits.

However, many people choose insurance amounts based only on their financial situation at the time of enrollment, without considering future uncertainties. Later, when circumstances suddenly change, the premiums become burdensome.

Then they visit the insurance company to cancel the policy—only to discover that they will receive back barely half of what they paid.

At that point, most customers seem to choose one of two options.

The first is deciding to endure the burden and continue paying until the principal is eventually recovered.

The second is deciding to cancel immediately, accepting the financial loss because current circumstances are too difficult.

Naturally, both situations are frustrating.

If people can afford it, most tend to choose the first option. But is that truly the correct decision?

Think about it carefully again.

Earlier, it was explained that surrender values are low because only the remaining balance after deducting loading premiums and risk premiums is returned. Furthermore, because some loading premiums are amortized in advance, additional unrecoverable losses occur, making the surrender value even smaller.

As time passes, interest accumulates on the savings premiums, creating the illusion that the original principal is gradually being restored.

But the extinguished portions—the loading premiums and risk premiums consumed before reaching breakeven—can never actually be recovered.

From a pure savings perspective, this can be an extremely inefficient decision.

In fact, it may be more rational to cancel the policy immediately, deposit the surrender value into a bank account, and simply save the equivalent monthly premium independently. Doing so could allow the principal to recover much faster while at least reducing the ongoing losses from continuously consumed risk premiums and loading premiums.

To be absolutely clear, canceling insurance based solely on the premiums already paid is undeniably a financial loss.

However, canceling a policy in order to establish a proper risk management plan—or to create a more effective savings strategy—can clearly become a financial benefit for the customer.