Episode 7 : 금융의 신자유주의

산업이 고도화되면서 사회에는 더 많은 돈이 필요하게 되었습니다. 돈의 발행이 금의 가치에 묶여 있을 때에는 돈의 증가량이 일정한 수준에 머물 수밖에 없었지만 미국의 부채를 기준으로 돈을 발행하게 되면서부터는 금의 양에 구애받지 않게 되었겠지요.

그런데 그렇다고 미국이 세계에 필요한 돈을 무한정 찍어낼 수는 없는 일입니다. 산업화의 속도와 사람들이 편리한 생활을 추구하는 것에 비례해 돈도 더 많이 필요할 텐데, 돈이 부족하면 큰 일이겠지요?

그래서 몇 가지 꼼수(?)를 부리기로 합니다.

그것이 바로 세계적인 신자유주의 기조와 맞물려 2008년 미국 발 금융위기의 시발점이 된 “자산유동화” 전략입니다.

자산 유동화 전략을 쉽게 이야기하자면 이렇습니다.

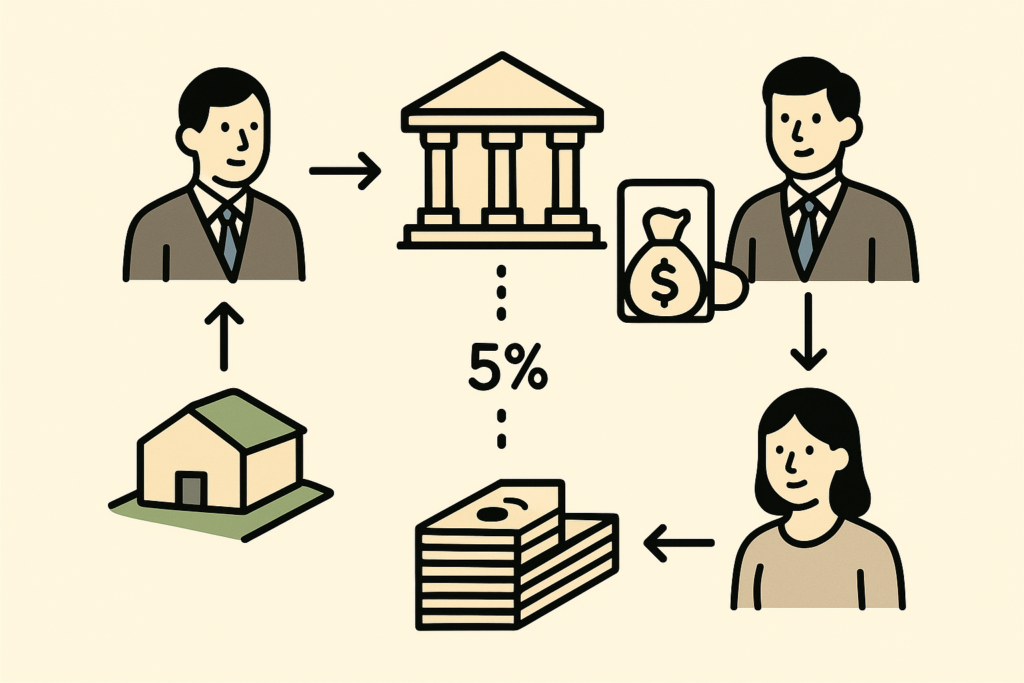

어떤 사람이 땅을 가지고 있습니다.

그런데 어느 날 사업자금을 마련하기 위해 땅을 담보로 은행에서 1억 원을 대출을 받았습니다. 은행은 땅을 담보로 제게 돈을 빌려주고 매년 5%의 이자를 받기로 했습니다.

그런데 이렇게 대출을 해 준 은행도 돈이 필요하게 되었습니다. 은행이 가진 돈은 대부분 저처럼 돈이 필요한 사람에게 대출을 해 주었기 때문에 더 빌려줄 돈이 없습니다.

그러자 은행이 묘안을 내 놓습니다. 바로 저에게서 대출 이자를 받을 수 있는 권리를 다른 사람에게 1억 원에 팔기로 한 것입니다.

제게서 5%의 이자를 받을 권리가 있는 은행이 이 대출증서를 사는 사람에게 자신들이 받아야 할 5%의 이자를 주기로 하고 팔아서 또 다시 1억 원의 현금을 확보합니다. 이 거래의 결과로 은행은 이익이 없는 장사를 하는 것처럼 보이지만 땅을 담보로 대출해 준 1억 원을 손 쉽게 회수한 것이지요.

실제로 다른 문제가 없다면 부동산과 같은 비유동성 자산을 현금으로 손쉽게 바꾸어 주는 이런 방법을 통해 은행은 무한정 필요한 돈을 만들어 낼 수 있을 것입니다. 만일 경제가 지속적으로 상승하고 이자를 갚아야 하는 저와 같은 사람들의 신용에 문제가 발생하지 않는다면 은행은 아무런 문제없이 돈 장사를 지속할 수 있겠지요?

마치 피라미드 금융사기 같은 일이 벌어지고 있지만 정상적인 거래가 이루어 지는 동안에는 아무런 일이 없습니다. 오히려 필요한 돈을 쉽게 조달하는 방법이므로 사회의 발전에도 기여하고 경기 부양에도 좋은 일이 되겠지요.

———————–

Financial Neoliberalism in the Modern Economy | Asset Securitization Dynamics

As industrial sophistication increases, society demands a larger monetary base. When currency issuance was tied to the value of gold, money supply growth inevitably stayed limited. However, once issuance was anchored to U.S. federal debt, it became detached from the physical constraint of gold reserves.

Yet the United States cannot print unlimited amounts of currency simply because the world requires more liquidity. As industrialization accelerates and lifestyles become more convenient, the demand for money rises proportionally, and a shortage of available capital would create systemic problems.

This led to a series of financial maneuvers. Aligned with a global neoliberal trajectory, these mechanisms produced the “asset securitization” strategy that ultimately ignited the 2008 U.S.-centered financial crisis.

Asset securitization operates as follows.

An individual owns a parcel of land. One day, to secure business capital, that individual obtains a 100 million KRW loan from a bank using the land as collateral. The bank extends the loan against the collateral and agrees to receive 5% annual interest.

However, the lending bank also faces its own funding shortage. Most of its capital is already committed to borrowers in need, leaving insufficient liquidity for additional loans.

The bank then devises a tactic: it sells the right to receive the borrower’s future interest payments to a third party for 100 million KRW.

The bank promises the buyer of the loan certificate the 5% interest it would have collected, thereby recovering 100 million KRW in cash. While this appears to be a zero-profit transaction, the bank has effectively and effortlessly recovered the original principal it lent, thanks to the collateralized loan.

If no complications arise, this method allows a bank to convert illiquid assets—such as real estate-backed loans—into cash at will. As long as the economy continues expanding and borrowers like this individual do not experience credit deterioration, banks can continue financial operations without disruption.

Although this system resembles a pyramid-like financial construct, no issues emerge as long as transactions proceed normally. In fact, because it provides an efficient means of sourcing capital, it supports economic development and contributes positively to broader economic stimulation.