평준식 위험보험료와 자연식 위험보험료

위험보험료를 산정하는 방식에는 평준식 위험보험료법과 자연식 위험보험료법이 있습니다.

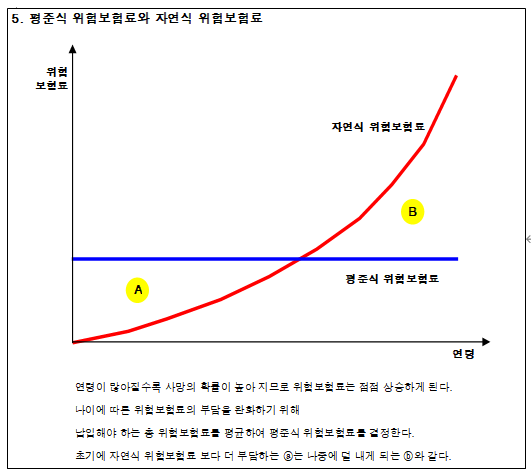

사람이 사망할 확률은 통상 나이가 많을수록 높아지게 마련이므로 정확하게 보험료를 산정한다면 젊을 때는 사망확률이 낮으므로 보험료를 적게 받고 나이가 들면 보험료를 많이 받는 것이 공평하겠지요? 이것이 자연식 위험보험료입니다.

그런데 평생을 보장하는 종신보험의 경우 나이가 들수록 보험료가 기하급수적으로 늘어나 결국에는 보험료를 납입하지 못할 수도 있습니다. 보험을 유지할 수 없는 것이지요.

그래서 총 기간 동안 납입해야 하는 금액을 평균하여 가입 당시에는 조금 더 내더라도 평생 납입할 수 있는 일정한 금액으로 보험료를 책정하는 데 이것이 평준식 위험 보험료법입니다.

그러다 보니 초기에 필요한 금액보다 더 납입한 부분이 쌓여 해지환급금을 형성하게 되는 것이지요. (이해를 돕기 위해 풀어 낸 이야기이며, 계리가 꼭 이렇지는 않습니다.)

대부분의 보험이 평준식 위험보험료를 적용하고 있지만, 변액유니버설보험과 같은 장기 투자상품은 초기에 투자되는 금액을 늘리기 위해 자연식 위험보험료를 적용하기도 합니다. (계속)

—————

Level Premium Risk Cost vs Natural Premium Risk Cost

There are two methods for calculating risk premiums: the level premium method and the natural premium method.

Since the probability of death generally increases with age, a strictly accurate premium calculation would charge lower premiums when individuals are young—due to lower mortality risk—and higher premiums as they age. This approach is known as the natural premium risk cost method.

However, in the case of whole life insurance that provides lifetime coverage, premiums would increase exponentially with age under the natural premium method, potentially reaching a point where the policyholder can no longer afford to pay. In other words, maintaining the policy becomes difficult.

To address this, insurers average the total amount payable over the entire coverage period. Even if the policyholder pays slightly more at the beginning, the premium is fixed at a consistent level that can be maintained throughout life. This is known as the level premium risk cost method.

As a result, the excess amount paid in the early years—beyond the actual required cost—accumulates and forms the basis of the surrender value. (This explanation is simplified for ease of understanding and may not fully reflect actuarial practices.)

While most insurance products apply the level premium method, long-term investment-oriented products such as variable universal life insurance may adopt the natural premium method to allocate more funds toward investment in the early stages. (To be continued)