Episode 23 : 수익률이 서민을 죽인다.

금융상품의 수익률을 표시하는 방법은 꽤 많습니다.

보통 기간수익률, 연 환산 수익률 그리고 실질수익률이라는 것이 있고, 이자를 부가하는 방법에 따라 단리와 복리로 구분하기도 합니다. 그런데 금융기관에서 제시하는 수익률이 항상 같은 기준으로 표현될까요?

우리가 금융기관을 거래할 때 가장 고민하는 것이 바로 수익률이지만, 이 수익률이 정확히 무엇을 의미하는 지에 대해 아는 분이 그리 많지 않은 것 같습니다. 그저 이 상품의 세전 수익률(이자소득세 15.4%를 떼기 전의 수익률)은 몇 %라고 나와 있는 것을 기준으로 상품을 선택하기 마련입니다.

그런데 이 수익률이라는 것에 매우 큰 함정이 숨어 있습니다.

바로 수익률을 기간수익률로 표시하느냐, 연 환산 수익률로 표시하느냐 아니면 실질수익률로 표시하느냐에 따라 다르게 나타난다는 것입니다.

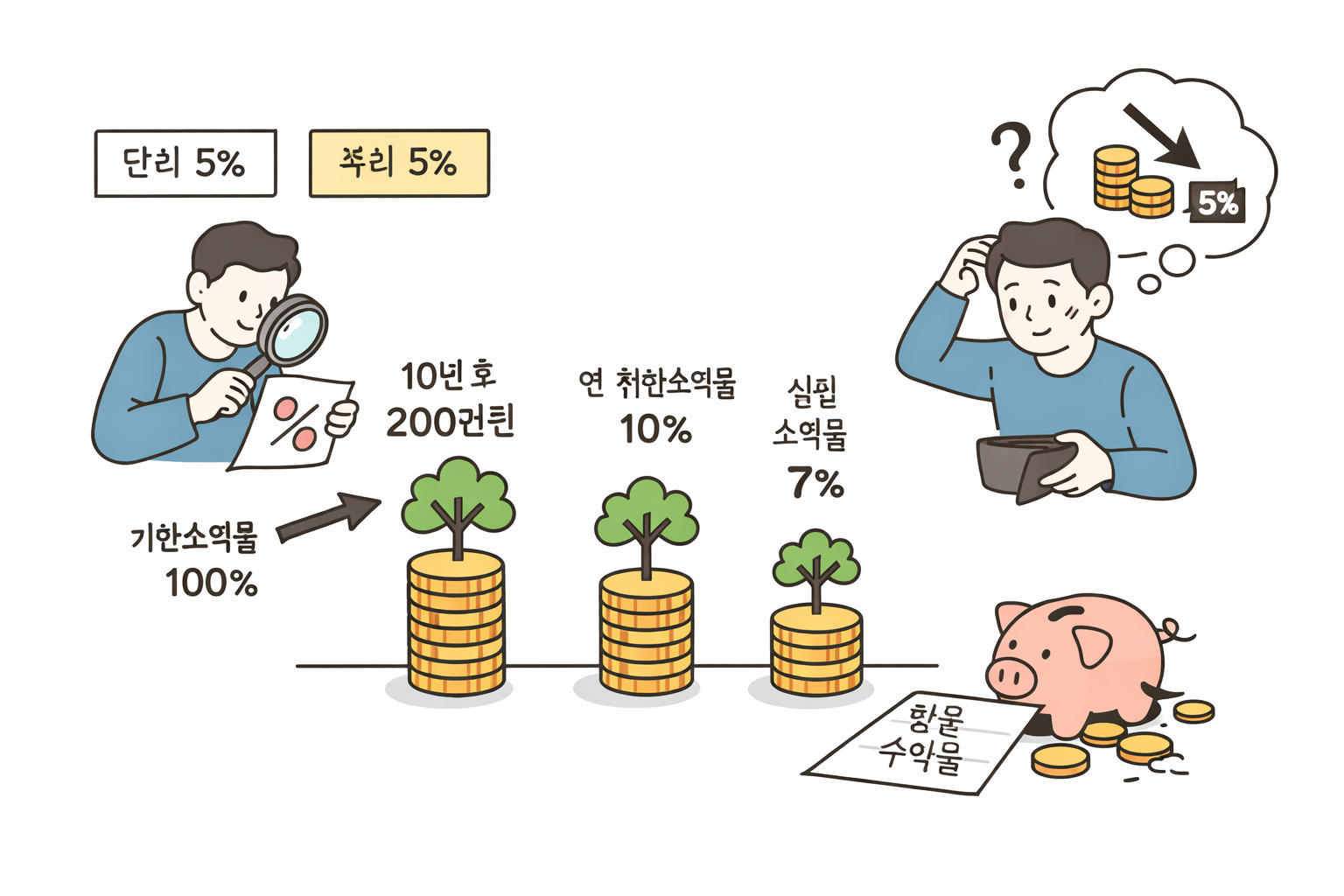

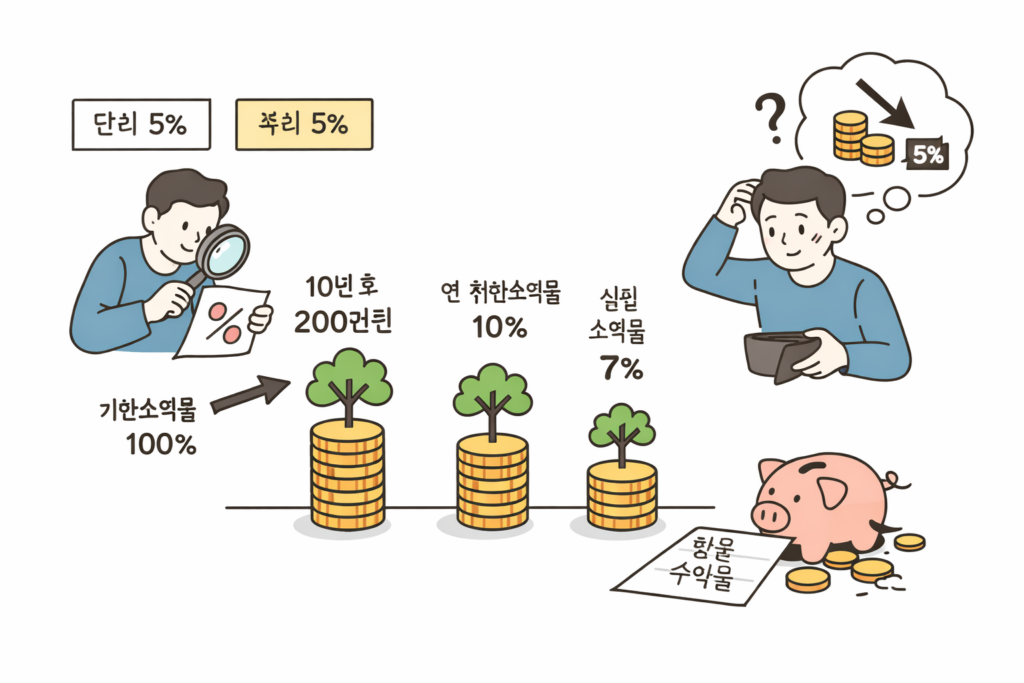

만일, 100만원을 투자하여 10년 만에 200만원이 되었다면 기간수익률은 10년에 100%가 됩니다.

연환산수익률은 이를 10년으로 나누어 연10%가 되지만, 실질수익률(내부수익률)은 약 7%정도입니다.

똑 같은 상품이지만 표현하는 방법에 따라 매우 큰 차이가 나는 수익률을 과연 우리가 알 수 있을까요? 특히 매월 돈을 불입하는 적금 상품과 목돈을 넣어두는 예금의 경우 이자를 지급하는 방법이 다르기 때문에 단리와 복리라고 표현하는 데 이는 계산방법이 완전히 다르기 때문에 서로 비교할 수 없는 개념이기도 합니다.

은행에서 매월 10만원씩 1년 동안 적금을 하기로 했습니다. 적금의 이자는 단리로 지급하기 때문에 매월 붙는 이자는 그저 한 켠에 쌓이기만 합니다. (이자를 원금에 더하여 다시 이자를 주는 방법은 복리계산법입니다.)

일년에 5%의 이자를 준다는 적금에 가입하면 10만원에 대한 이자는 일년에 5,000원입니다. 첫 달에 불입한 10만원은 1년 동안 저축이 될 것이므로 5,000원의 이자를 받게 되지만, 그 다음 달에 저축한 10만원은 11개월만 저축되므로 5,000원/12개월x11개월 하여 4,583원의 이자가 지급됩니다.

제일 마지막 달에 저축한 10만원은 겨우 한 달만 저축되어 있었으니 417원의 이자가 붙는 것이지요. 이렇게 1년 동안 낸 원금은 120만원이고, 그 동안 붙은 총 이자는 32,500원입니다. 상품의 이자율이 5%라고 했지만 실제 수익률은 32,500원/120만원x100%는 2.71%인 것이지요.

만일 이 돈을 5% 단리의 적금이 아니라 5%의 복리를 준다는 상품에 가입했다면 받을 수 있는 이자는 33,001원으로 단리보다 조금 높은 이자를 받게 되겠고 실제 수익률은 2.75%로 소폭 올라가겠지만 5%의 확정이자를 복리로 주는 은행의 적금상품은 존재하지 않습니다. (복리를 적용하는 상품은 매월 불입하는 적금이 아니라 목돈을 넣어두는 예금이나 아니면 투자상품입니다.)

그래서 금융기관 별로 제시하는 서로 다른 기준의 수익률을 비교하여 가입상품을 결정하는 것은 매우 바보스러운 짓이 되는 것이지요. 열심히 찾고 골라서 운 좋게도 물가 상승율을 상회하는 이자를 준다는 금융상품에 가입했는데, 실제로는 전혀 그렇지 않다는 것을 나중에야 알게 된다면 얼마나 바보 같은 짓입니까? 하지만 많은 금융소비자들이 실제로 이런 비교를 하고 있으니 슬픈 일이 아닐 수 없습니다.

——————–

Episode 23: Rate of Return Kills the Ordinary People

There are quite a few ways to express the rate of return of financial products.

Typically, there are period return, annualized return, and real return. Depending on the method used to add interest, it may also be classified as simple interest or compound interest. But are the returns presented by financial institutions always expressed according to the same standard?

When dealing with financial institutions, the factor people worry about most is the rate of return. However, it seems that not many people actually know what this return precisely means. Most simply choose products based on the pre-tax return rate of the product (the return before the 15.4% interest income tax is deducted).

But there is a very large trap hidden within this concept of return.

The return can appear completely different depending on whether it is expressed as a period return, an annualized return, or a real return.

For example, if 1,000,000 won is invested and becomes 2,000,000 won after 10 years,

the period return is 100% over 10 years.

If this is divided over 10 years, the annualized return becomes 10% per year.

However, the real return (internal rate of return) is approximately 7%.

Even though it is exactly the same product, the rate of return varies greatly depending on how it is expressed. Can we really recognize such differences? In particular, installment savings where money is deposited monthly and fixed deposits where a lump sum is deposited use different methods of paying interest. These are often described as simple interest and compound interest, but because the calculation methods are entirely different, they are concepts that cannot be directly compared.

Suppose you decide to deposit 100,000 won every month into a savings account for one year.

Since installment savings accounts pay interest using simple interest, the interest earned each month simply accumulates separately. (The method of adding interest to the principal and calculating interest again is called compound interest.)

If you subscribe to a savings product that pays 5% interest annually, the interest on 100,000 won is 5,000 won per year. The first 100,000 won deposited will remain in the account for a full year, so it earns 5,000 won in interest. However, the 100,000 won deposited in the following month is saved for only 11 months, so the interest becomes 5,000 won ÷ 12 months × 11 months, which equals 4,583 won. The final 100,000 won deposited in the last month remains for only one month, so it earns just 417 won in interest.

In this way, the total principal deposited over the year becomes 1,200,000 won, and the total interest earned during that period is 32,500 won. Although the product advertises an interest rate of 5%, the actual return is 32,500 won ÷ 1,200,000 won × 100%, which equals 2.71%.

If this money had been invested in a product offering 5% compound interest instead of 5% simple interest, the interest earned would be 33,001 won—slightly higher than simple interest. The actual return would increase slightly to 2.75%. However, there is no bank installment savings product that guarantees a fixed 5% compound interest. (Products that apply compound interest are not installment savings accounts where money is deposited monthly, but rather fixed deposits where a lump sum is placed or investment products.)

For this reason, comparing financial products based on different standards of return presented by financial institutions and then choosing a product accordingly is actually a very foolish act. Imagine spending a great deal of effort searching for a financial product that appears to offer a return higher than the inflation rate, only to realize later that the reality is completely different. How foolish would that be? Yet many financial consumers are in fact making such comparisons, which makes it a rather unfortunate situation.