Episode 27: 대출금에 이름표가 있다고?

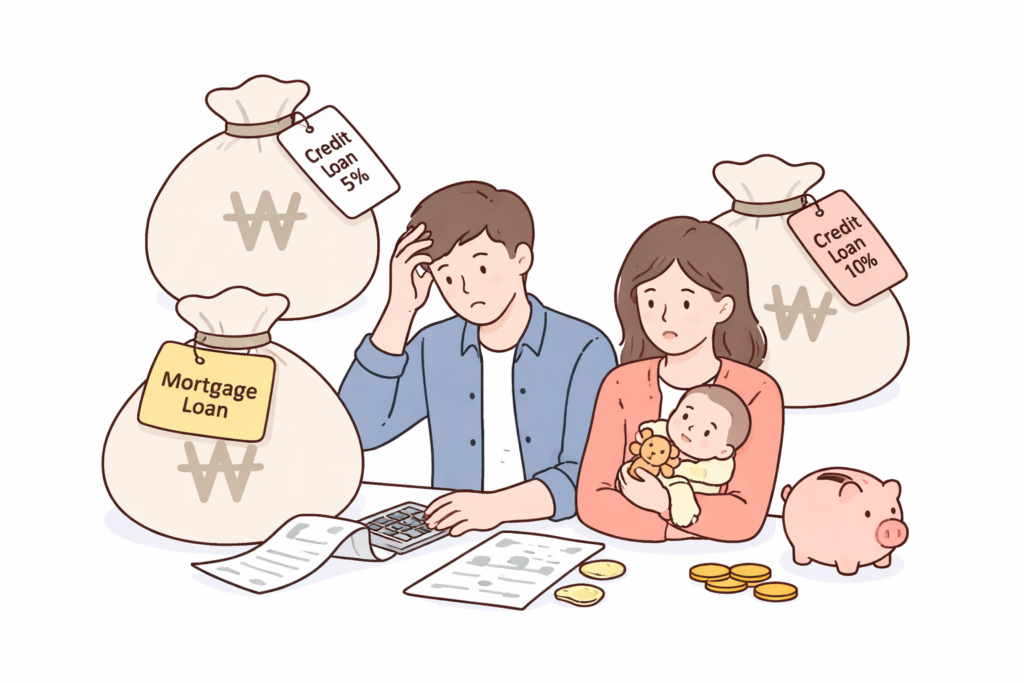

어떤 분이 집을 사려고 1억 원을 대출받았습니다.

엄마가 그랬습니다. 결혼하면 집부터 사라고 말이지요. 엄마의 말은 틀린 적이 없습니다. 그래서 조금 부담스럽지만 대출을 받아 집을 사고 열심히 갚기로 했습니다. 덕분에 매달 생활비가 조금 부족하지만 빨리 갚고 마음 편하게 살려고 아끼고 아껴서 매달 백 만원씩 10년 동안 열심히 갚자고 아내와 약속했습니다.

그런데 아이가 태어나고 시간이 지나면서 아내가 힘들어합니다. 월급은 똑같은데 쓸 돈은 자꾸 늘어나니 힘든가 봅니다. 결국 매월 적자가 나는 가계부 때문에 천 만원의 신용대출을 받았습니다.

집을 사며 받은 담보대출의 이자는 5%였는데, 신용대출의 이자는 10%라는군요. 같아야 하는 대출이 자꾸 늘어나니 부담스럽고 불안합니다. 이것도 빨리 갚아주어야 하는 데, 이제 담배도 끊고 친구들 모임도 줄이고, 아내한테도 더 아껴 쓰자고 얘기해야 할 것 같습니다. 집을 사기 위해 대출을 받을 때는 참 즐거웠는 데, 모자란 생활비를 대출받으려니 참 부끄럽습니다.

이 이야기에는 대출에 대한 아주 중요한 편견이 숨어 있습니다.

그것은 대출의 종류와 용도를 구분하여 이름표를 붙이는 것에서 시작합니다. 대출금을 일부러 주택담보대출과 신용대출로 구분할 필요가 있을까요? 또 집을 사기 위해 빌린 돈과 생활비로 빌리는 돈을 구분할 필요가 있을까요? 생활비로 빌리는 돈은 이자가 비싸기도 하고, 이 때문에 돈 관리를 잘못하고 있다는 자괴감도 생길 테고, 우선적으로 갚아야 한다고 생각할 수 있습니다.

하지만 과연 집을 사기 위해 빌린 담보대출금은 집에 대한 빚이고, 생활비가 부족해 빌린 신용대출금은 생활에 대한 빚일까요?

담보대출이든 신용대출이든 대출은 필요할 때 요긴하게 쓰려고 받는 것인데, 집을 사기 위해서든 생활비로 쓰기 위해서든 빌린 돈은 어쨌든 빌리는 순간 내 재산 어딘가에 “부채”라는 이름으로 숨어버리고 만다는 것을 아셔야 합니다. 눈이 없는 이 놈은 맑은 물에 떨어뜨린 먹물처럼 퍼져 다시 꺼낼 수 없다는 말입니다.

결국 대출은 어떤 용도이든, 어떤 종류이든 받는 순간 어딘가로 숨어버리고, 눈앞에 보이는 것은 그저 대출금을 갚아가는 상환 조건뿐 이란 것을 이해하셔야 합니다. 집을 사기 위한 용도로 대출받는 것과 생활비로 쓰기 위해 대출받는 것을 구분하는 것이 결국 실상 별 의미 없는 일이라는 것입니다.

주택담보대출은 10년 동안 매월 백 만원씩 갚아야 하는 대출이고, 신용대출은 1년 동안 10%의 이자만 내지만 1년 후에 갚아야 하는 대출입니다.

그런데 만일 처음 주택담보대출을 매월 50만원씩 20년을 갚기로 했다면 어떨까요? 매월 50만원의 상환만 하면 되니 생활에 대한 부담도 좀 덜 테고, 10%의 이자를 내야 하는 신용대출을 안 받아도 되니 이자 부담도 좀 덜지 않았을까요? 어차피 다른 일이 없다면 이 집에서 평생 살 테니 말입니다. 아니 혹시 다른 집으로 이사를 한다면 나의 대출금은 새로운 주인이 해결할 일이니 말입니다.

대출금에는 이름표가 없습니다.

대출을 받았다면 이를 어떻게 유리하게 상환하고 그러면서 가족의 생활에도 문제없이 관리할 것인지에 집중하는 것이 대출에 대한 올바른 관리방법이라는 것입니다.

————-

Episode 27: Do Loans Come with Labels?

Someone took out a loan of 100 million won to buy a house.

His mother had always told him to buy a house first when getting married. His mother had never been wrong. So, although it felt burdensome, he took out a loan, bought a house, and decided to repay it diligently. As a result, their monthly living expenses became somewhat tight, but he promised his wife that they would save as much as possible and repay 1 million won every month for 10 years so they could live more comfortably afterward.

However, after their child was born and time passed, his wife began to struggle. Their income remained the same, but expenses kept increasing. Eventually, due to a monthly deficit in their household budget, they took out an additional credit loan of 10 million won.

The mortgage loan they took out to buy the house had an interest rate of 5%, but the credit loan carried an interest rate of 10%. As the total amount of debt continued to grow, it became increasingly burdensome and anxiety-inducing. Now, he feels that this loan must also be repaid as quickly as possible. He considers quitting smoking, reducing social gatherings with friends, and asking his wife to cut back on spending even more. While taking out a loan to buy a house once felt exciting, borrowing money for living expenses now feels embarrassing.

There is a very important misconception about loans hidden in this story.

It begins with labeling loans based on their type and purpose.

Is it really necessary to distinguish loans as mortgage loans and credit loans? Is it necessary to separate money borrowed for purchasing a house from money borrowed for living expenses? Loans taken for living expenses usually have higher interest rates, which may lead to feelings of guilt and the belief that one is mismanaging money. As a result, people tend to think these loans must be repaid first.

But is a mortgage loan truly a “debt for the house,” while a credit loan is a “debt for living expenses”?

Whether it is a mortgage loan or a credit loan, borrowing is simply a tool used when needed. Regardless of whether the money is borrowed to buy a house or to cover living expenses, the moment it is borrowed, it becomes part of your financial liabilities under the label of “debt.” This debt does not remain separate—it spreads like ink dropped into clear water, making it impossible to isolate again.

In the end, regardless of its purpose or type, once a loan is taken, it becomes part of an overall financial obligation. What remains visible is not the purpose of the loan, but the repayment conditions. Distinguishing between loans for housing and loans for living expenses ultimately has little practical meaning.

A mortgage loan may require monthly repayments of 1 million won for 10 years, while a credit loan may require only interest payments at 10% for one year, with the principal due at the end of the term.

But what if, from the beginning, the mortgage loan had been structured to require monthly payments of 500,000 won over 20 years instead? The reduced monthly burden could have eased daily living expenses and potentially eliminated the need for a high-interest credit loan. After all, if there are no major changes, the borrower is likely to live in that house for a lifetime. And even if they move, the responsibility for the remaining loan may be transferred to the new owner.

Loans do not come with labels.

Once you take out a loan, the key is not to categorize it by purpose, but to focus on how to repay it efficiently while maintaining a stable and sustainable household life.