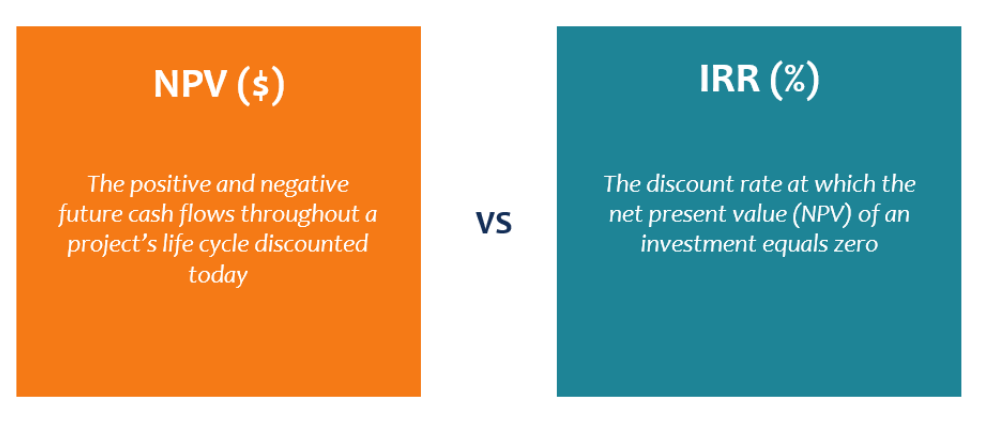

- 내부수익률(IRR, Internal Rate of Return)

내부수익률(IRR)은 말 그대로 기업 내부적으로 투자여부를 결정하기 위해 사용하는 수익률이다. 따라서 IRR은 투자금에 투자 수익률이고 기회비용 차원에서 최대한 받을 수 있는 이자 수익률이기도 하다. 그러나 IRR은 실질 이자율이 아닌 투자여부를 결정하는데 사용되는데, 현재의 투자금과 예상되는 수익의 현재가치를 동일하게 해주는 기준점인 것이다. 그리하여 IRR이 가중평균 자본비용인 WACC보다 크면 투자를 집행하고, 작으면 투자하지 않는다.

IRR은 현금흐름표에서 엑셀함수를 사용해서 쉽게 구할 수 있다. 구하는 방법은 뒤에 별도로 예시를 통해 설명하겠다. 일반적으로 회사의 재무팀은 산업 평균적이거나 기업내부상황에 적정한 WACC의 기준율을 가지고 있다. 중소기업의 경우 없다면, 회사의 자기자본과 차입금을 고려하여 재무상황에 맞게, 미리 설정을 해두면 앞으로의 사업을 위한 투자 경제성 평가를 손쉽게 할 수 있어 좋을 것이다.

- 순현재가치(NPV, Net Present Value)

현재 투자한 금액으로 발생할 수 있는 미래 수익의 현금흐름을 현재가치(Present Value)로 환산해서 비교해야 투자 경제성을 평가할 수 있다. 즉, 현재 투자한 금액으로 사업을 하여, 미래에 수익으로 들어오리라 예상되는 현금흐름 금액을 내부수익율(IRR)로 할인한 것이 현재가치(PV)가 된다. IRR로 할인한 PV는 만약 투자금을 화장품 사업에 사용하지 않고, 은행이나 다른 금융기관을 이용해서 투자했을 경우에 대한 기회비용을 차감한 현재가치를 의미한다.

그리하여 실제 투자한 금액에서 PV를 차감한 금액을 순현금증감액인 NPV(Net Present Value)라 한다. 따라서 ‘NPV=0’이면, 실투자금과 미래수익의 현재가치가 똑같다는 것을 의미하므로, 투자여부의 판단은 NPV가 0보다 커야 투자의 가치가 있는 것이고, 0보다 작다면 투자할 가치가 없는 것이다. NPV를 구하는 방법도 현금흐름표에서 엑셀함수를 이용하여 쉽게 구할 수 있으므로, 다음에 나올 예시를 통해 설명하겠다.

———————-

Internal Rate of Return (IRR)

The Internal Rate of Return (IRR) is literally the rate of return used internally by a company to decide whether or not to proceed with an investment. Therefore, IRR represents the return on investment and also the interest rate that could be earned as the opportunity cost. However, IRR is not the actual interest rate but is used to determine whether to proceed with an investment by finding the rate that equates the present value of the expected returns with the initial investment. If the IRR is greater than the Weighted Average Cost of Capital (WACC), the investment is made; if it is lower, the investment is not pursued.

IRR can be easily calculated using an Excel function from the cash flow statement. The method of calculation will be explained separately with an example later. Generally, a company’s finance team has a standard WACC rate that is either industry-average or appropriate for the company’s internal situation. For small and medium-sized enterprises, if such a standard does not exist, it would be beneficial to set one in advance based on the company’s equity and debt. This would make it easier to evaluate the economic feasibility of future business investments.

Net Present Value (NPV)

To evaluate the economic feasibility of an investment, it is necessary to compare the present value (PV) of the future cash flows that could be generated from the current investment. In other words, PV is the amount obtained by discounting the future cash flows expected to be generated from the business with the IRR. The PV discounted by IRR represents the present value after subtracting the opportunity cost that would be incurred if the investment were made in a bank or another financial institution instead of the cosmetics business.

The amount obtained by subtracting the PV from the actual investment amount is the Net Present Value (NPV). Therefore, if “NPV = 0,” it means that the present value of the future returns equals the actual investment, indicating that the investment decision should only be made if the NPV is greater than 0. If the NPV is less than 0, the investment is not worthwhile. The NPV can also be easily calculated using an Excel function from the cash flow statement, and this will be explained in the following example.