Episode 19 : 금융의 비교우위

비교우위라는 말이 있습니다. 기술 수준이 높지만 인건비가 비싼 나라와 인건비는 저렴하지만 농업이 발달한 나라가 서로 무역을 한다면 어떤 일이 벌어질 까요?

인건비가 비싼 나라는 같은 돈으로 가격이 저렴한 농산품을 생산하는 것 보다는 첨단산업이 집약된 고가의 기계를 만드는 데 경쟁력이 있고, 인건비가 저렴한 나라는 같은 돈으로 더 많은 농산품을 생산할 수 있습니다. 따라서 두 나라간의 경제를 비교해 보면 앞의 나라는 기계류의 생산에, 뒤의 나라는 농산품의 생산에 각각 비교우위가 있다고 합니다.

앞에서 살펴보았듯이 금융은 각기 다른 역사적 배경을 가지고 시작되었습니다. 서로 다른 목적과 서로 다른 이유로 시작되었으니 그 거래의 내용도 분명히 다르고 따라서 전문분야도 따로 있습니다. 그럼에도 불구하고 우리는 금융에 대해 세부적인 사항을 잘 모르고 거래하는 경향이 있습니다. 각 기관의 비교우위에 대해 제대로 이해하지 못하고 있기 때문에 혼란이 가중되는 것이지요.

금융기관은 일반적으로 사기업이지만 공공기관의 성격이 매우 강합니다. 전통적으로 은행은 예대금리차 수익으로, 증권회사는 거래수수료 수익으로, 보험회사는 부가보험료 수익으로 운용된다고 이야기했습니다.

물론 최근 금융기관의 영역파괴로 은행에서 펀드와 저축성 보험을 판매한다든가 증권회사가 지급결제 기능을 갖는다든가 하는 일이 허용되며 다양한 수익원을 창출하고 있지만, 전통적인 수익원(은행의 예대마진, 증권회사의 거래 수수료, 보험회사의 부가보험료)의 비율은 2~3% 수준입니다.

이 금액은 매출에 대한 이익이므로 여기에서 운영비용과 세금 등을 제하면 더욱 낮아 지겠지요. 그렇다면 이 정도의 수익을 폭리라고 할 수는 없을 것입니다. 그래서 금융기관이 공공기관에 가까운 것이지요.

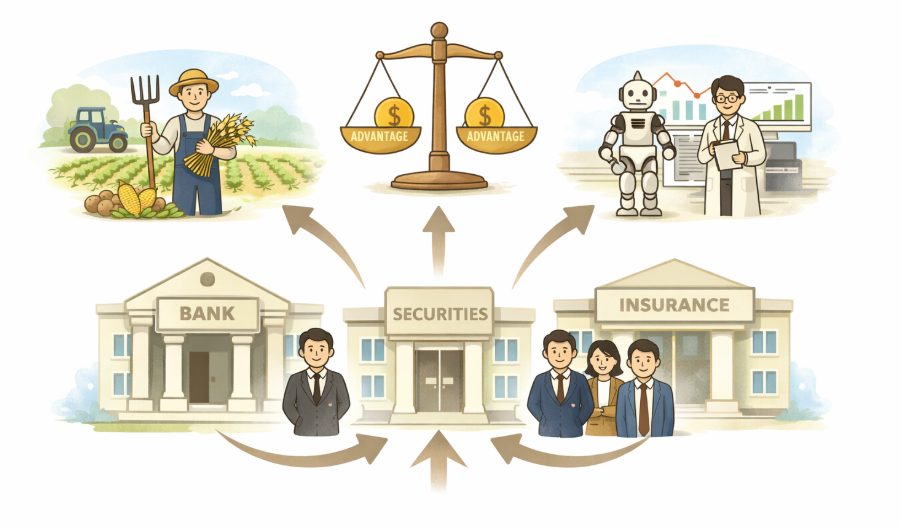

은행은 예금과 대출을 거래할 수 있는 금융기관이고, 증권은 투자의 중개인 역할을 하는 금융기관이며, 보험은 상조회로 운영되는 금융기관이므로 우리는 이를 어떤 목적으로 어떻게 거래하는 것이 효율적인 지에 대해 연구해야 합니다.

서로 비슷해 보이지만 완전히 다른 상품을 거래해야 하므로 공부도 필요하지만, 분명한 것은 각 금융기관별로 비교우위가 확실히 있다는 것입니다.

은행의 예금보다 더 안정적이고 수익률이 높은 상품이 증권회사에 존재하지만 은행의 대출상품보다 더 좋은 대출상품을 판매하는 금융기관은 없으므로, 은행은 대출상품의 거래에 비교우위가 있습니다. 증권회사보다 더 안정적이고 수익률이 높은 투자시스템을 갖춘 회사는 없기에 증권회사는 수익을 바라는 투자상품의 거래에 비교우위가 있지요.

보험회사는 서로의 부조와 장기거래 상품에 효과적인 상품을 판매하고 있으므로 이런 상품이 필요하다면 보험회사와 거래하는 것이 옳습니다. 따라서 우리는 각 기관의 비교우위에 대해 정확히 알고 이를 활용해야만 합니다.

그렇지 않다면 공공기관에 가까운 금융회사가 잘 모르는 고객들을 상대로 더 많은 이익을 추구하려고 할 테니까 말입니다. 만일 그런 일이 발생한다면 어떻게 될까요?

실제로 그런 일이 무척 많이 발생하고 있음에도 불구하고 우리는 잘 모릅니다. 왜냐하면 그런 일들에 대해 사전에 알 수 있는 방법도 별로 없고, 안다고 해도 조직적으로 대항할 힘이 없습니다. 그런데 얼마 전 정말 황당한 일이 벌어졌지요. 바로 미국에서 벌어진 “월가를 점령하라” 사건입니다.

처음 소셜 네트워크 상에서 한 사람이 주장한 이 운동이 전 세계적 금융소비자 저항운동으로 들불처럼 번지며 각 국의 금융기관들이 골머리를 앓았습니다. 하지만 저는 이런 운동이 결정적인 효과를 가져오리라고 생각하지 않습니다. 왜냐하면 금융의 핵심적인 구조에 대해 잘 모르는 성난 군중들의 요구에 금융기관은 그저 생색내기용 정책을 내고 말 것이기 때문입니다.

분명한 것은 이런 운동보다 더 중요한 것이 바로 모든 사람들이 금융기관의 허와 실에 대해 분명히 알고 이에 따른 개인의 이익 추구에 최선을 다 할 때 금융기관이 크게 변화할 것이라는 믿음입니다.

현명한 금융소비자라면 가급적 금융 비용을 줄이는 거래를 할 것이고, 이에 대해 금융기관은 정당한 이익을 확보하려는 경영을 할 때 서로 상생할 수 있는 방법이 도출되지 않을까요? 그러기 위해 우선 우리가 알아야 하는 것이지요. 이제 편견을 깨기 위한 다양한 내용에 대해 검토해 보도록 하겠습니다. (계속)

—————-

There is a concept called comparative advantage. What would happen if a country with a high level of technology but expensive labor costs trades with a country where labor costs are low but agriculture is highly developed?

A country with expensive labor costs has greater competitiveness in producing high-value, technology-intensive machinery rather than producing low-priced agricultural products with the same amount of money. On the other hand, a country with low labor costs can produce a larger quantity of agricultural products with the same amount of money.

Therefore, when comparing the economies of the two countries, the former has a comparative advantage in the production of machinery, while the latter has a comparative advantage in the production of agricultural goods.

As examined earlier, finance began with different historical backgrounds. Since it originated for different purposes and reasons, the nature of the transactions is clearly different, and thus each sector has its own area of specialization.

Nevertheless, people often tend to engage in financial transactions without understanding the details. Confusion is intensified because people do not properly understand the comparative advantages of each financial institution.

Financial institutions are generally private enterprises, but they possess very strong characteristics of public institutions. Traditionally, banks operate on profits generated from the interest margin between deposits and loans, securities companies operate on profits from transaction commissions, and insurance companies operate on profits from additional insurance premiums.

Of course, with the recent breakdown of boundaries within the financial industry, banks are now allowed to sell funds and savings-type insurance products, and securities companies have been given payment and settlement functions, thereby creating diverse revenue sources.

However, the proportion of traditional revenue sources—banks’ interest margins, securities companies’ transaction commissions, and insurance companies’ additional insurance premiums—remains around 2–3 percent.

Since this amount represents profit relative to revenue, the figure becomes even smaller after operating expenses and taxes are deducted. Therefore, it would be difficult to describe this level of profit as excessive profiteering. This is precisely why financial institutions are often considered close to public institutions.

Banks are financial institutions that conduct deposit and lending transactions, securities firms are financial institutions that act as intermediaries for investment, and insurance companies are financial institutions that operate on the principle of mutual aid. Therefore, we must study how and for what purposes it is most efficient to engage in transactions with them.

Although they may appear similar, they actually deal with completely different products. This requires learning and understanding, but what is clear is that each type of financial institution has a distinct comparative advantage.

There are investment products at securities companies that can be more stable and generate higher returns than bank deposits. However, there are no financial institutions that offer loan products superior to those provided by banks.

Therefore, banks possess a comparative advantage in lending products. Since there are no companies with investment systems more stable and profitable than those of securities firms, securities companies have a comparative advantage in investment products aimed at generating returns.

Insurance companies provide products that are effective for mutual aid and long-term contractual arrangements. Therefore, if such products are needed, it is appropriate to conduct transactions with insurance companies. Accordingly, we must accurately understand the comparative advantages of each institution and make use of them.

Otherwise, financial companies—which are close to public institutions—may attempt to pursue greater profits from customers who lack sufficient knowledge. What would happen if such situations arise?

In fact, such situations occur quite frequently, yet we are often unaware of them. This is because there are few ways to detect such practices in advance, and even if we become aware of them, we lack the collective power to respond effectively. However, not long ago, a truly astonishing event occurred. It was the “Occupy Wall Street” movement that took place in the United States.

What began as a claim by a single individual on social networks spread like wildfire into a global movement of financial consumer resistance, causing financial institutions around the world considerable concern.

However, I do not believe that such movements will produce decisive results. This is because financial institutions will likely respond to the demands of angry crowds—who may not fully understand the fundamental structure of finance—with merely symbolic policies.

What is clear is that something more important than such movements is for everyone to clearly understand the strengths and weaknesses of financial institutions and to pursue their own interests accordingly. When individuals act based on such understanding, financial institutions will inevitably undergo significant change.

A wise financial consumer will try to conduct transactions in ways that minimize financial costs. If financial institutions, in response, manage their operations in a way that secures legitimate profits, would it not be possible to derive a mutually beneficial solution?

For that to happen, there are things we must first understand. Now, let us examine various topics that will help break existing misconceptions. (To be continued)