Episode 29: 올바른 대출 전략

대출은 잘 관리만 한다면 매우 큰 이익을 주는 활동이라는 데 동의하십니까? 그렇다면 어떻게 해야 대출을 잘 관리하며 이익을 볼 수 있을까요?

앞서 말씀드린 대로 돈은 태어나는 순간부터 이미 빚을 안고 태어납니다. 평생 돈과 함께 살아가는 우리는 이미 빚에서 자유로울 수 없는 삶을 사는 것입니다. 오히려 빚을 잘 이용하는 법을 터득하는 것만이 빚에서 자유로워질 수 있다는 역설이 통하는 시대임을 기억하십시오.

효율적인 부채활용을 위해 몇 가지 전략이 필요합니다.

(1) 장기 대출을 받아라.

살아가는 과정 자체가 부채에서 자유로울 수 없다면 아예 처음부터 장기 대출을 받는 것이 옳지 않을까요? 장기 대출은 장기간 상환해야 하는 빚이므로 비교적 이자율이 저렴하고 원리금 상환에 대한 부담이 적습니다.

집을 사기 위해 대출을 받는 경우를 생각해 보지요. 예전에는 없었지만 지금은 30년 만기 모기지론(Mortgage Loan)을 받을 수도 있지요. 하지만 집을 사고 30년 동안 빚을 갚아야 한다는 것이 많은 분들에게 큰 부담으로 작용하는 것 같습니다.

하지만 달리 생각해 본다면 집은 평생 가지고 있을 장기자산이므로 오랫동안 저렴하게 주거비용을 부담하는 것이 합리적이고 바른 생각일 것입니다. 만일 이 부담이 싫어서 빨리 갚으려 한다면 이 때문에 매월 써야 하는 생활비에 부담이 생겨 생활이 위축될 것이고, 이 부담은 결국 다른 형태의 빚으로 나타날 가능성이 높습니다.

장기간의 대출계약에는 큰 잇점이 있습니다.

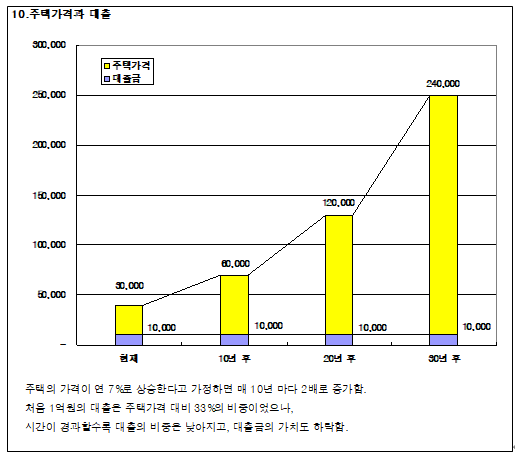

만일 집의 가격이 연 7%의 수익률로 상승하고, 대출금리가 5%의 고정금리라면 이 계약을 이행하는 동안 아래 그림과 같이 대출금과 매월 상환해야 하는 돈의 실제 가치는 감소하지만 반대로 집의 가치는 계속 상승하여 대출의 부담이 지속적으로 줄어들게 된다는 것입니다.

30년 동안 이자만 납입한다고 하면 최초에 자산대비 부채비율 이 33%였지만 30년 후에는 4.2%로 줄어들게 될 겁니다. 이것이 바로 이자의 효과입니다. (주택가격이 지속적으로 상승한다는 가정 하에 그렇다는 말입니다. 만일 주택가격이 떨어질 것이라면 집을 사는 것 자체를 심각하게 고려해야 하겠습니다.)

원금을 빨리 상환하는 것 보다는 이자 납입을 통해 지속적으로 대출금을 쓸 수 있는 권리를 확보하고 나머지 여유자금을 5% 이상의 수익을 낼 수 있는 곳에 투자하는 것이 효과적이겠지요.

또한 빌린 돈의 장기상환을 통해 대출금의 상환부담을 줄이고 충분한 생활비를 확보하여 돈 때문에 궁핍하지 않은 생활을 하는 것도 중요한 사항일 겁니다.

쉽게만 생각해 온 대출에도 전략이 필요합니다. 어떠한 경우에도 장기대출을 받는 것이 효율적이란 것을 기억하십시오.

감당할 수 있는 조건을 설정하라.

아무리 대출을 효율적으로 활용한다 하더라도 감당할 수 있는 범위 내에서 활용해야 합니다. 개인이 감당할 수 있는 대출에는 다음의 두 가지 조건이 있습니다.

첫 번째는 적정한 부채비율의 설정입니다.

최근에는 무분별한 주택담보대출을 규제하기 위해 LTV(Loan to Value Ratio: 담보대출비율)를 적용합니다. 이것은 담보의 가치에 대해 대출 가능한 금액을 규제한다는 이야기인데요, 자기 돈에 비해 너무 많은 대출을 받는 것을 막고 규제하여 신용의 위험을 줄이자는 것입니다.

전체적으로 자기자본 대비 약 100% 이내 (내 돈이 10억 원이면 10억 원의 대출)면 안전하다고 보는 것 같습니다만, 자기자본의 약 50%선 (내 돈이 10억 원이면 5억 원의 대출), 즉 총자산대비 약 30%정도의 부채비율(내 돈 10억 원과 대출금 5억 원을 합하여 15억 원이 총자산이므로 5억원의 대출은 약 33%의 부채비율입니다.) 이 적정한 것 같습니다.

10억 원짜리 집을 산다면 5억 원까지는 대출을 해 줄 수 있지만 적정한 금액은 3억 원 정도일 것이라는 말입니다.

——————–

Episode 29: The Right Loan Strategy

Do you agree that loans can generate significant benefits if managed properly? If so, how can we manage loans effectively to maximize gains?

As mentioned earlier, money is inherently tied to debt from the moment it is created. Since we live our entire lives with money, we cannot be completely free from debt. In fact, it is a paradox of modern finance that only by learning how to use debt effectively can we truly become free from it.

To utilize debt efficiently, several strategies are required.

Take out long-term loans.

If life itself cannot be separated from debt, wouldn’t it be better to start with long-term borrowing from the beginning? Long-term loans are repaid over extended periods, which typically results in lower interest rates and reduced pressure on principal and interest payments.

Consider the case of taking out a loan to buy a house. In the past, such options were limited, but today it is possible to obtain a 30-year mortgage loan. However, the idea of repaying debt for 30 years can feel burdensome to many people.

From another perspective, however, a house is a long-term asset that one may hold for a lifetime. Therefore, spreading out housing costs over a long period at a lower rate can be seen as a rational and sound financial decision. If one tries to repay the loan too quickly due to psychological discomfort, it may create pressure on monthly living expenses, leading to a reduced quality of life. This burden may eventually manifest as other forms of debt.

Long-term loan agreements offer significant advantages.

If housing prices increase at an annual rate of 7% while the loan interest rate is fixed at 5%, then over time, the real value of the loan and the monthly repayment burden decreases, while the value of the house continues to rise. This results in a gradual reduction in the overall burden of the loan.

For example, if only interest is paid over 30 years, an initial debt-to-asset ratio of 33% could decrease to approximately 4.2% after 30 years. This is the effect of interest and asset appreciation. (This assumes that housing prices continue to rise. If prices are expected to fall, purchasing a house itself should be carefully reconsidered.)

Rather than focusing on rapid principal repayment, it is often more effective to maintain the right to use borrowed funds by paying interest while investing surplus funds in opportunities that yield returns higher than 5%.

In addition, reducing repayment pressure through long-term borrowing and securing sufficient living expenses to avoid financial strain is also an important consideration.

Even loans, which may seem simple, require strategic planning. It is important to remember that, in most cases, long-term loans are more efficient.

Set manageable conditions.

No matter how effectively loans are utilized, they must remain within manageable limits. There are two key conditions for sustainable borrowing.

The first is setting an appropriate debt ratio.

Recently, regulations such as the Loan to Value (LTV) ratio have been introduced to control excessive mortgage lending. This limits the amount that can be borrowed based on the value of the collateral, helping to prevent excessive borrowing relative to one’s own capital and reducing credit risk.

In general, a debt level within 100% of one’s equity (e.g., borrowing 1 billion won with 1 billion won of personal capital) is often considered safe. However, a more conservative and appropriate level would be around 50% of equity. For example, if you have 1 billion won of your own capital and borrow 500 million won, your total assets would be 1.5 billion won, resulting in a debt ratio of approximately 33%, which is considered a reasonable level.

In other words, if purchasing a house worth 1 billion won, while it may be possible to borrow up to 500 million won, a more appropriate loan amount would be around 300 million won.