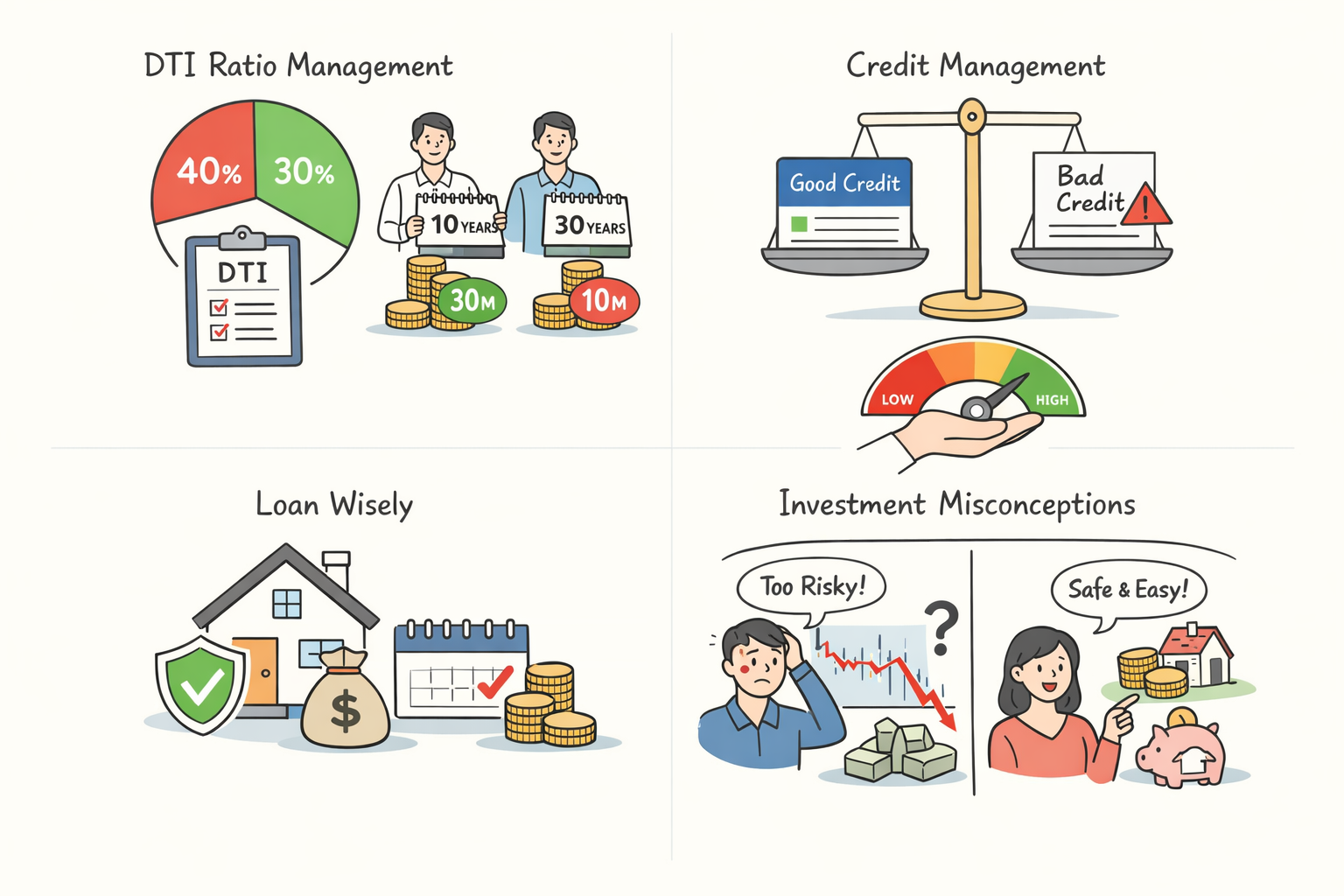

두 번째는 적정한 부채상환비율의 설정입니다.

총 수입에서 얼마를 부채상환에 쓰는 것이 적정한가를 보는 지표인데요, DTI(Debt to Income: 총부채상환비율)라고 하여 상환해야 하는 대출의 원리금이 연 수입의 40% 이하이면 안전하다고 보는 것 같습니다만, 다른 지출을 고려하면 30% 이내로 설정하는 것이 적정한 것 같습니다.

3억 원의 대출을 10년 동안 갚기로 한다면 매년 약 3천 만원씩 상환하는 꼴이므로 연 수입이 적어도 1억 원은 되어야 하지만 30년 동안 갚기로 한다면 매년 1천 만원씩 상환하는 수준이므로 연 수입이 3천 만원을 넘으면 받을 수 있다는 이야기입니다. 즉, DTI는 부채의 상환기간과 밀접한 관련이 있는 지표입니다.

은행이 제시하는 LTV와 DTI의 조건은 대출의 건전한 활용을 위한 최대 한도를 제시한 것이지 적정한 선을 제시한 것은 아니라고 보여집니다. 가급적이면 두 기준 이내에서 내게 맞는 적정선을 찾는 것이 필요하며 그 한도 내에서 대출을 활용하는 것이 안전할 것입니다.

신용관리에 최선을 다하라.

대출에 관한 생각을 하면 반드시 짚어야 하는 것이 바로 신용에 대한 이야기입니다.

신용은 보통 자산이 많고 수입이 많을수록 우수할 것이라고 판단하지만 실제로는 그 보다 더 중요한 것이 바로 그 이후에 보이는 약속의 이행과정입니다. 적정한 금액을 대출받고 있는가, 정해진 날짜에 원리금을 입금하고 있는가 등의 거래이력이 개인의 신용도를 정하는 데 매우 중요한 사항이 되고 있습니다.

신용이 우수하면 더 낮은 금리를 적용 받게 되고, 더 많은 대출 한도가 주어지는 등 은행과의 거래에서 좋은 조건을 제시 받을 수 있습니다. 반대로 신용이 나빠지면 은행은 언제든지 대출금의 상환을 요구할 수도 있고, 대출의 연장을 거부할 수도 있으며, 가산금리가 적용되거나 각종 불이익을 받을 수도 있습니다.

어차피 빚을 안 지고 살 수 없는 삶이라면 위에 열거한 대로 가급적이면 장기대출을 적은 부담으로 지고 가는 것이 최선입니다. 대출 거래에 대한 적은 부담이 상환에 대한 부담뿐 아니라 윤택한 삶의 측면에서 훨씬 유리할 것이고, 아울러 개인의 신용 관리에도 큰 도움이 될 것이므로 부채의 현명한 활용법에 대해 충분히 연구하는 것이 필요합니다.

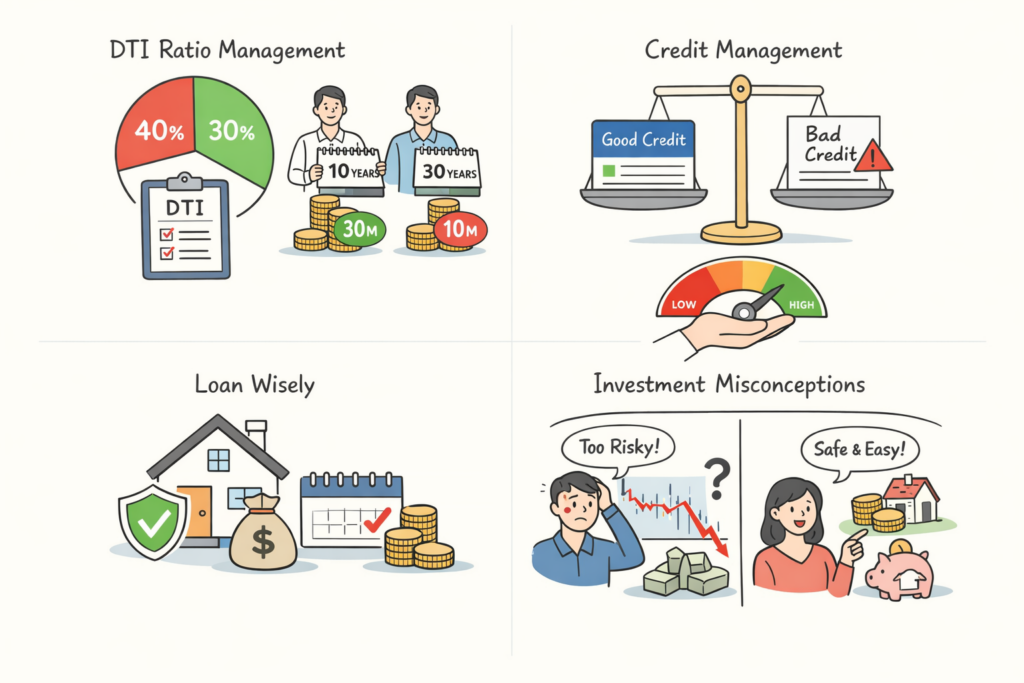

* 투자에 대한 오해와 편견

“증권회사는 투자한 돈의 원금보존도 안되고,

주변에 주식 하다가 망한 사람도 많아서 위험한 것 같고,

너무 어려워서 왠지 제가 갈 수 있는 곳이 아닌 것 같아요.”

“그럼 투자는 어디에 하시지요?”

“부동산이나 예금 같은 것에 투자하지요.”

물론 증권회사의 투자 상품들은 일반인들이 접근하기 어려울 수도 있고, 가격의 변동성이 큰 것이 사실입니다. 그렇지만, 앞서 이야기했듯 증권회사처럼 안정적인 투자시스템을 가진 회사가 있나요? 투자에 대해 잘못 알고 있기 때문에 투자가 어려운 것입니다.

투자란 쌀 때 사서 비쌀 때 팔아 이익을 내는 행위입니다. 투자하는 중에는 반드시 가격의 등락이 있고, 투자가 잘 되어 수익이 나든 잘못되어 손실을 보든 투자의 책임은 투자자에게 있다고 합니다. 그러니 이런 불안하고 위험한 투자는 아무래도 하고 싶지 않겠지요.

하지만 투자하지 않고 수익을 낼 수 있는 방법이 있을까요? 단연코 이제는 그럴 수 있는 방법은 없습니다. 그리고 투자가 위험하다고 하는 것은 투자와 투기를 구분하지 못하는 것입니다. 투자에 대한 우리의 습관적인 거부감도 매우 큰 문제입니다.

이제 투자에 대한 오해와 편견에서 벗어나 효율적이고 쉬운 투자 방법을 찾아야 합니다.

The second is the establishment of an appropriate debt repayment ratio.

This is an indicator that determines what portion of total income should be allocated to debt repayment. It is commonly referred to as DTI (Debt to Income ratio), and it is generally considered safe when the annual principal and interest repayment obligation is within 40% of annual income. However, when accounting for other expenditures, it is more appropriate to set this ratio within 30%.

For example, if a loan of 300 million KRW is to be repaid over 10 years, the annual repayment would amount to approximately 30 million KRW. In this case, an annual income of at least 100 million KRW would be required. On the other hand, if the same loan is repaid over 30 years, the annual repayment would be around 10 million KRW, meaning that an annual income exceeding 30 million KRW would suffice to qualify. In other words, DTI is an indicator that is closely related to the loan repayment period.

The LTV and DTI conditions presented by banks represent the maximum limits for the sound utilization of loans rather than optimal benchmarks. Therefore, it is necessary to identify a suitable level within these limits that aligns with one’s financial situation, and utilizing loans within that range would be considered safe.

Make every effort to manage your credit.

When discussing loans, credit is an essential factor that must be addressed. Credit is often assumed to be higher when assets and income are greater, but in reality, what matters more is the consistency in fulfilling financial obligations thereafter. Transaction history—such as whether one has borrowed an appropriate amount and whether principal and interest payments are made on time—plays a crucial role in determining an individual’s creditworthiness.

With strong credit, one can benefit from lower interest rates and higher borrowing limits, as well as more favorable terms in dealings with banks. Conversely, if credit deteriorates, banks may demand immediate repayment, refuse loan extensions, apply higher interest margins, or impose various disadvantages.

If living without debt is not a realistic option, the best strategy is to carry long-term debt with minimal financial burden, as outlined above. Lower financial strain in loan transactions not only reduces repayment pressure but also contributes to a more comfortable standard of living. Additionally, it significantly aids in maintaining personal credit. Therefore, it is essential to thoroughly study and understand the prudent use of debt.

- Misconceptions and Biases About Investment

“Securities firms do not guarantee the principal of invested funds,

and I’ve seen many people around me fail after investing in stocks,

so it seems risky. It also feels too complicated, like something beyond my reach.”

“Then where do you invest?”

“I invest in real estate or savings products.”

Certainly, investment products offered by securities firms may be difficult for the general public to access, and it is true that they involve significant price volatility. However, as mentioned earlier, are there any institutions with a more structured and stable investment system than securities firms? Investment appears difficult largely because it is misunderstood.

Investment is the act of buying at a low price and selling at a higher price to generate profit. During the investment process, price fluctuations are inevitable, and regardless of whether the investment yields profit or loss, the responsibility ultimately lies with the investor. Naturally, such uncertainty and perceived risk may discourage participation.

However, is there any way to generate profit without investing? In today’s environment, such methods essentially do not exist. Furthermore, labeling investment as inherently risky often stems from a failure to distinguish between investment and speculation. Our habitual aversion to investment is also a significant issue.

It is now necessary to move beyond these misconceptions and biases and seek efficient and accessible methods of investing.