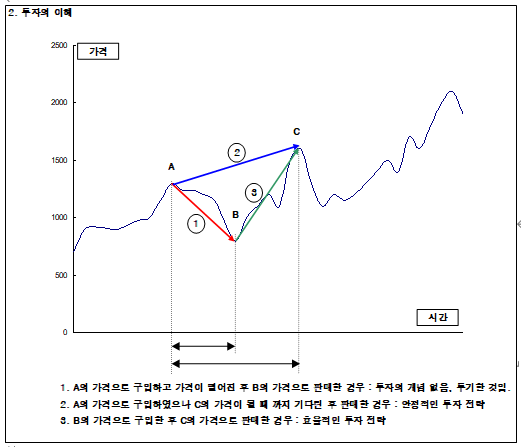

Episode 31: 투자와 투기를 구분할 수 있다고?

어떤 분이 1억 원이 있어 금을 사 두었습니다. 그런데 금 가격이 자꾸 떨어집니다. 지금 팔아야 하는 지 아니면 갖고 있어야 하는 지 고민을 하다가 저에게 어떻게 할 지를 묻습니다.

정답은 “지금 그 돈이 필요한가?“ 입니다.

돈이 필요하다면 손해를 보더라도 당장 팔아야 하는 것이고, 그렇지 않다면 오를 때까지 기다려야 하는 것이지요.

어느 분이 한 달 정도를 쓸 수 있는 돈으로 주식을 샀다고 생각해 봅시다. 이 분은 “한 달 뒤에는 100% 오른다.”는 정보를 믿고 투자하셨는데 갑자기 가격이 50%로 폭락했습니다. 드디어 한 달이 지나고 이 돈을 써야 하는 시점에서 어찌해야 할까요? 50%로 손해난 주식을 팔아야 합니다. 죽고 싶겠지요?

어떤 분도 똑같이 그 주식을 샀습니다. 그런데 이 분은 이 돈을 3년이건 5년이건 당분간 쓸 계획이 없습니다. 처음 한 달은 50% 손해가 났는데, 꾸준히 오르기 시작하더니 5년 만에 투자금의 100% 수익이 났네요. 5년에 100%라면 산술적으로 1년에 약 20%(복리로는 14% 정도)의 수익을 냈다는 말이지요?

실상 투자해서 사 둔 물건의 현재 가격은 의미 없는 가격일 뿐입니다. 이것을 팔아서 돈으로 바꾸어야 실제가격이 되는 것이지요.

만일 우리가 가격이 오를 때까지 기다릴 수 있다면 투자를 통해 손해를 볼 일은 절대 없는 것이지요. 문제는 기다리지 못하게 하는 요인에 있습니다. 만일 언제까지 갚아야 하는 남의 돈으로 투자하거나, 사용 시한이 정해져 있는 돈으로 투자했다면 기다릴 수 없겠지요?

갚아야 하는 남의 돈으로 투자하거나, 사용 시한이 정해져 있는 돈으로 투자했다면 기다릴 수 없습니다. 기다릴 수 있는 시간이 주어지지 않은 투자는 투자가 아니라 단연코 투기입니다. 우리의 투자 패러다임을 바꾸지 않으면 절대 투자수익을 볼 수 없습니다.

많은 분들이 가격의 변동이 큰 상품에 투자하는 것은 위험하다라고 생각합니다. 그런데 가격이 꾸준히 느리게 상승하는 상품에 투자하는 것과 매 순간 가격 변동이 매우 심한 상품에 투자하는 것 중 어느 것이 투자수익이 클까요?

가격변동이 심하다면 싸게 살 수 있는 기회도 많아지고, 비싸게 팔 수 있는 기회도 많아지겠지요? 그렇다면 높은 투자수익을 얻기 위해 적정한 상품은 가격 변동이 매우 심한 상품이겠지요?

만약 장기간 쓸 수 있는 여유자금으로 가격 등락이 큰 상품에 투자한다면 우리는 얼마든지 쌀 때 사서 비쌀 때 팔 수 있으니 이익을 볼 확률이 매우 높습니다. 원금의 손실은 걱정 없이 이렇게 안전하고 훌륭한 투자가 어디 있습니까? 당신께서 전문 Trader가 아니라면 여유자금으로 장기투자 해서 손해 볼 일은 100% 없습니다. 오히려 큰 이익을 볼 일만 있는 것이지요.

—————–

Episode 31: Can You Really Distinguish Between Investment and Speculation?

Someone has 100 million KRW and purchased gold. However, the price of gold keeps declining. They are unsure whether to sell now or hold, so they ask for advice. The answer is simple: “Do you need the money right now?” If the money is needed, it should be sold immediately, even at a loss. If not, it should be held until the price rises.

Now consider someone who invested in stocks using money intended for one month of living expenses. This person believed information claiming that “the price will double in one month,” but instead, the price suddenly dropped by 50%. When one month passes and the money is needed, what should be done? The stock must be sold at a 50% loss. It would feel devastating.

Another person bought the same stock, but this individual has no need to use the money for 3 to 5 years. In the first month, the investment also dropped by 50%, but then it gradually recovered and, after five years, generated a 100% return. A 100% return over five years translates to approximately 20% per year in simple terms (about 14% annually on a compound basis).

In reality, the current market price of an investment asset is merely a nominal value. It only becomes a realized value when the asset is sold and converted into cash. If we can wait until prices rise, there is effectively no reason to incur a loss through investment.

The problem lies in the factors that prevent us from waiting. If the investment is made with borrowed money that must be repaid by a certain date, or with funds that have a fixed usage timeline, waiting becomes impossible.

An investment without sufficient time to wait is not an investment—it is speculation. Without changing our investment paradigm, it is impossible to achieve meaningful returns.

Many people believe that investing in assets with high price volatility is risky. However, between assets that increase slowly and steadily and those that fluctuate significantly in price, which offers greater potential returns? High volatility creates more opportunities to buy at low prices and sell at high prices. Therefore, assets with significant price fluctuations can offer higher investment returns.

If one invests in highly volatile assets using surplus funds available for the long term, it becomes entirely possible to buy low and sell high, significantly increasing the probability of profit. Without the concern of principal loss, such an approach represents a highly effective and safe investment strategy. Unless you are a professional trader, investing long-term with surplus funds does not lead to losses—in fact, it only creates opportunities for substantial gains.