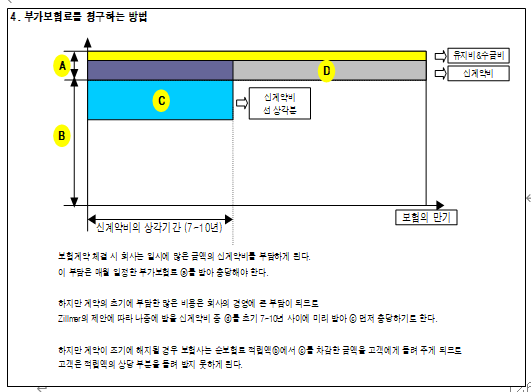

부가보험료의 선상각

상조회에 새로운 고객이 가입을 하면 총무는 그가 고객이 되기에 알맞은 사람인지 심사도 하고 새롭게 고객으로 등록하는 등 가입 초기에 각종 비용을 쓰게 됩니다. 특히 대수의 법칙에 따라 상조회는 많은 회원이 가입해야 안정성이 확보되기 때문에 회원 가입을 권유한 사람(보험설계사)에게 보상을 하게 되고 이로 인해 초기에 필요한 비용이 생각보다 많이 들어가게 되는 것이죠.

하지만 회원이 내는 매월의 보험료는 이에 비해 턱없이 부족하여 독일의 질멜 (Zillmer)이라는 사람이 부가보험료 선상각 법을 제안하게 됩니다. 즉, 상조회에 가입하는 사람은 오랫동안 회비를 낼 것이므로 매월 일정한 비용을 받으나 초기에 조금 많은 비용을 받고 나중에 조금 적은 비용을 받으나 똑 같은 것 아닌가? 라는 생각에서 시작된 제도입니다.

실제로 매월 100만원의 보험료를 내는 어떤 저축성 보험 상품은 가입하는 순간에 이미 700만원의 비용을 쓰게 되는 구조를 가지고 있습니다. 이 돈을 초기 7년 동안 나누어 받기로 함으로써 고객은 가입하는 때부터 일년에 약 100만원씩 비용을 갚아줘야 하는 의무를 갖게 되는 것이지요.

물론 이 방법은 고객이 오랫동안 상조회의 회원일 것이라는 가정이 들어맞을 때는 매우 이상적인 방법이겠지만 만일 짧은 기간 안에 회원이 상조회를 탈퇴하는 일이 생긴다면 상조회는 미리 써버린 돈을 회원에게 돌려받을 수 없게 되어 손해를 보게 되고, 회원은 이미 납입한 보험료를 전액 돌려받을 수 없게 되어 거래의 두 주체 모두가 손해를 보는 상황에 직면하게 되는 것입니다.

모든 보험회사들이 고객으로부터 받을 부가보험료 중 신계약비를 먼저 쓰기 때문에 발생하는 이런 문제들이 바로 고객의 불신을 초래하는 주요한 원인입니다.

그래서 보험은 반드시 고객의 필요에 의해 가입하고, 장기간 유지해야 서로 이익인 상품입니다.

보장성 보험과 저축성 보험의 구분

통상 우리나라에서는 순보험료의 위험보험료와 저축보험료의 비율을 기준으로 보장성 보험과 저축성 보험을 구분합니다. 즉, 위험보험료의 비율이 50%를 넘으면 보장성 보험이고, 저축보험료의 비율이 50%를 넘으면 저축성 보험이라고 구분하는 것이지요.

실제로 대표적인 보장성 보험인 종신보험과 정기보험은 순보험료의 100%가 위험보험료로 구성되어 있고, 소득공제상품인 연금저축보험은 순보험료의 100%가 저축보험료로 구성되어 있습니다.

그런데 한 가지 짚고 넘어가야 할 것이 있습니다.

위험보험료는 보험금으로 지급되는 돈이므로 돌려받지 못한다고 했는데 종신보험의 경우 기간이 지나면 해지환급금이 생기게 되지요? 해지환급금은 저축보험료를 모아 주는 돈이라고 했는 데 저축보험료가 전혀 없는 종신보험에 해지환급금이 있다는 말은 좀 이상하지 않습니까? (계속)

———————

Advance Amortization of Loading Premium

When a new customer joins a mutual aid association, the administrator incurs various initial costs, such as evaluating whether the individual is suitable to become a member and registering them as a new customer.

In particular, based on the law of large numbers, the association must secure a large number of members to maintain stability, so compensation is provided to the person who recommended the new member (insurance agent). As a result, the initial costs tend to be higher than expected.

However, the monthly premium paid by members is relatively insufficient to cover these initial expenses, which led a German actuary, Zillmer, to propose the method of advance amortization of loading premiums.

This concept is based on the idea that since members will pay premiums over a long period, it makes little difference whether a higher portion of the cost is collected in the early stage and less later, as long as the total remains the same.

In practice, a savings-type insurance product with a monthly premium of 1,000,000 KRW may incur an upfront cost of 7,000,000 KRW at the moment of subscription. By amortizing this amount over the first seven years, the customer effectively assumes the obligation to repay approximately 1,000,000 KRW per year in costs from the beginning of the contract.

Of course, this method works ideally if the assumption that the customer will remain a member for a long period holds true. However, if a member withdraws within a short period, the association cannot recover the upfront costs already spent, resulting in a loss for the company. At the same time, the member cannot receive a full refund of the premiums already paid, leading to a situation where both parties incur losses.

These issues arise because insurance companies typically use the acquisition costs from the loading premium in advance, and this is one of the main causes of customer distrust.

Therefore, insurance is a product that should be subscribed to based on the customer’s actual needs and maintained over the long term for mutual benefit.

Distinction Between Protection-Type and Savings-Type Insurance

In general, in Korea, insurance products are classified into protection-type and savings-type based on the ratio of risk premium to savings premium within the net premium. If the proportion of the risk premium exceeds 50%, it is classified as protection-type insurance, whereas if the savings premium exceeds 50%, it is classified as savings-type insurance.

In practice, representative protection-type insurance products such as whole life insurance and term life insurance consist of 100% risk premium within the net premium. On the other hand, pension savings insurance, which is eligible for tax deductions, consists of 100% savings premium within the net premium.

However, there is an important point to consider.

It was stated that the risk premium is used for insurance payouts and therefore is not refundable. Yet, in the case of whole life insurance, a surrender value is generated after a certain period. Since the surrender value is formed from accumulated savings premiums, it seems contradictory that whole life insurance—which contains no savings premium—still provides a surrender value. (To be continued)