상호회사와 주식회사, 배당부 보험과 무배당부 보험

보험회사는 이익을 추구하지 않는 상조회라고 말씀 드렸고, 상호회사로 발전되어서도 이익과 손실을 고객에게 돌려준다고 했습니다. 보험회사는 부가보험료로 급여를 지급받고 있는 데 무슨 이익과 손실이냐고 생각할 지도 모르지만 한번 짚고 넘어가야 할 것 같습니다.

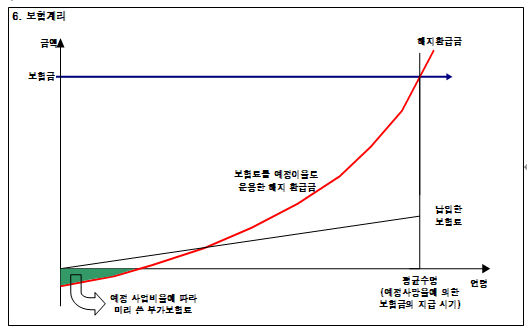

보험회사는 보험료를 결정할 때 보험금이 지급될 것으로 예상되는 시기(경험생명표로 예측한 평균수명)와 지급해야 하는 금액을 기준으로 매월 고객으로부터 받아야 할 보험료를 역산합니다. 여기에 또 중요한 인자가 바로 예정이자율이지요.

만약 대부분의 사람이 80세에 사망할 것이라고 예측되고, 사망 시 1억 원의 보험금을 지급해야 한다면 가입하는 시점부터 얼마씩을 받아야 회사가 80세 되는 해에 1억 원을 만들 수 있을 지를 계산하는 것입니다. (이를 보험계리라고 합니다.)

만일 시장의 이자율이 높다면 같은 보험료로 더 빨리 보험금을 만들어 낼 수 있고, 낮다면 어렵겠지요. 또 고객이 80세 이전에 사망한다면 손해를 볼 것이고, 이후까지 산다면 이익이 되겠지요. 또 한 가지는 회사가 처음 예상했던 운영비용이 생각보다 많이 들면 손해를, 덜 들면 이익을 볼 것입니다.

이를 예정이자율과 실제이자율의 차이에 따른 이차(손)익, 예정사망률과 실제사망율의 차이에 따른 사차(손)익, 예정사업비율과 실제사업비율의 차이에 따른 비차(손)익이라고 하는 데, 이런 이익과 손실이 발생하면 회사의 형태에 따라 처리하는 방법이 다릅니다.

상호회사는 상조회의 구조와 동일하기 때문에 손실이 발생하면 고객에게 이를 청구하고 이익이 나면 돌려주게 되어 있습니다. 이를 배당이라고 하는 데 통상 손실이 발생하여 고객에게 더 청구하지 않도록 보험료를 조금 더 받습니다. 남으면 돌려주는 게 비난을 피하는 방법일 테니까요.

주식회사는 회사가 경영의 책임을 지고 있기 때문에 손익이 발생해도 고객에게 청구하거나 돌려주지 않는 상품을 판매하고 있습니다.

여기에서 배당부 보험과 무배당부 보험이 생겨난 것이지요.

즉, 상호회사는 이익이 나면 고객에게 돌려주는 상품인 배당부 보험을 판매하고, 주식회사는 보험료를 조금 덜 받는 대신 이익이 나든 손실이 나든 회사가 책임을 지는 무배당부 보험을 판매하는 것이 원칙인데, 우리나라 보험회사는 오랫동안 주식회사임에도 불구하고 IMF 이전에는 배당부 보험을 판매했고, IMF 이후에 무배당부 보험으로 전환하였습니다.

여기에서 또 몇 가지 문제가 발생합니다.

예전에는 시장의 이자율이 10%가 넘는 고금리여서 보험회사들이 7.5%의 예정이율을 기준으로 보험료를 산출하고 상품을 판매했습니다. 당연히 고객의 돈으로 높은 수익이 발생하면 이 중 7.5%는 무조건 배당(수익률을 보증)하고 그 이상 되는 수익은 다른 이름으로 배당하기로 했습니다.

그리고 이렇게 예상되는 이익을 모두 배당할 경우를 가정해서 나중에 꽤 많은 금액을 돌려받을 수 있다고 광고하고 판매에 활용했지요. 그런데 시장의 이자율이 5% 미만으로 떨어지면서 보험회사는 장기적으로 7.5% 이상의 수익률은커녕 7.5%로 보증한 예정이자율도 감당하기 어려운 상황을 맞게 됩니다.

실제 이런 이유로 오랫동안 0%의 금리가 지속된 일본에서는 90년대에 닛산생명과 동방생명 등 여러 개의 대형 보험회사가 파산하기도 하였습니다.

그래서 서둘러 예정이율을 낮추거나 실세금리에 연동하는 이율을 적용하거나 수익률을 적용한(변액보험) 상품을 무배당부로 판매하게 된 것입니다. 요즘은 거의 보험회사로부터 배당 받을 수 있는 경우가 없습니다.

—————–

Mutual Companies vs Stock Companies, Participating vs Non-Participating Insurance

Insurance companies were originally described as mutual aid organizations that do not pursue profits, and even as they evolved into mutual companies, profits and losses are returned to policyholders. Although insurance companies receive compensation through loading premiums, it is still necessary to examine how profits and losses arise.

When determining premiums, insurance companies calculate the amount to be collected from customers by working backward based on the expected timing of insurance payouts (predicted life expectancy using mortality tables) and the payout amount. A key variable in this calculation is the assumed interest rate.

For example, if most individuals are expected to pass away at age 80 and a benefit of 100 million KRW must be paid at that time, the insurer calculates how much premium must be collected from the point of enrollment to accumulate that amount by age 80. This process is known as actuarial calculation.

If market interest rates are high, the insurer can accumulate the required payout more quickly with the same premium, whereas lower interest rates make it more difficult. Additionally, if a policyholder dies before age 80, the insurer incurs a loss, while survival beyond that age generates a gain. Operational costs also play a role—higher-than-expected expenses result in losses, while lower costs generate profits.

These differences are categorized as follows: gains or losses from discrepancies between assumed and actual interest rates (interest margin gain/loss), differences between assumed and actual mortality rates (mortality gain/loss), and differences between assumed and actual expense ratios (expense gain/loss). The way these gains and losses are handled depends on the type of insurance company.

In mutual companies, which maintain a structure similar to mutual aid associations, losses are charged to policyholders and profits are returned to them. This return is called a dividend. Typically, insurers collect slightly higher premiums to avoid charging additional amounts later if losses occur, and any surplus is returned to policyholders.

In contrast, stock companies assume full responsibility for management and therefore offer products where profits and losses are not passed on to policyholders. This distinction gives rise to participating and non-participating insurance.

In principle, mutual companies sell participating insurance policies that return profits to policyholders, while stock companies sell non-participating insurance policies that charge slightly lower premiums but retain all profits and absorb all losses. However, in Korea, despite being stock companies, insurers sold participating policies before the IMF crisis and transitioned to non-participating policies afterward.

Several issues emerged from this transition.

In the past, when market interest rates exceeded 10%, insurers calculated premiums based on an assumed interest rate of 7.5% and sold products accordingly. Naturally, when high returns were generated from customer funds, at least 7.5% was guaranteed as dividends, and any excess returns were also distributed under different forms of dividends.

Products were marketed by assuming these projected returns would be fully distributed, often promising substantial future payouts. However, as market interest rates fell below 5%, insurers faced a situation where even maintaining the guaranteed 7.5% return became difficult, let alone exceeding it.

In Japan, where near-zero interest rates persisted for an extended period, several large insurers such as Nissan Life Insurance and Toho Mutual Life Insurance went bankrupt in the 1990s due to these pressures.

As a result, insurers moved quickly to lower assumed interest rates, link them to market rates, or introduce products with investment-based returns (such as variable insurance), primarily offering them as non-participating policies. Today, it is rare for policyholders to receive dividends from insurance companies.