앞서 마케팅 예산 장에서, 나는 컨설팅 했던 M사의 광고 예산에 대해 언급한 바가 있다. 당시 M사가 놀라웠던 점은 모든 영수증과 세금계산서를 세무사에게 넘기고, 회사는 어느 누구도 재무회계적으로 신경도 안 쓴다는 것이었다. 심지어는 매출이 400억이나 되는 회사였는데도 그 흔한 회계직원 한 명 없었다.

그래서 M사는 매분기 부가세 신고와 매년 상반기 연말 결산자료를 세무사에만 의존해왔는데, 그 자료는 그저 과거에 대한 결론적인 수치일 뿐, 그 수치가 앞으로 사업적으로 변해야 할 방향을 제시하는 바를 아는 사람은 아무도 없었다. 그래서 나는 그 회사의 5개년 손익계산서를 엑셀로 한눈에 비교할 수 있도록 만들어서, 매출, 비용, 이익의 추이를 보고 과거 비용적인 문제점과 이익이 감소하는 원인에 대해 CEO에게 얘기했다. 그렇게 일목요연하게 보고 나서야 CEO는 깜짝 놀라며, 과다한 광고비를 줄이기로 결정했던 것이다.

이렇게 세무사에게만 의존하는 방식은 경영관리상 큰 문제가 있다. 세무사는 그저 세법적으로 문제가 없도록 국세청에 신고하는 기준으로 세무회계만 하기 때문이다. 그런데 사실 기업을 경영하기 위해선 재무회계와 관리회계가 더 중요한데, 세무사에게 맡기기만 하면 경영을 위한 회계는 하지 않는다는 것과 다름이 없는 것이다.

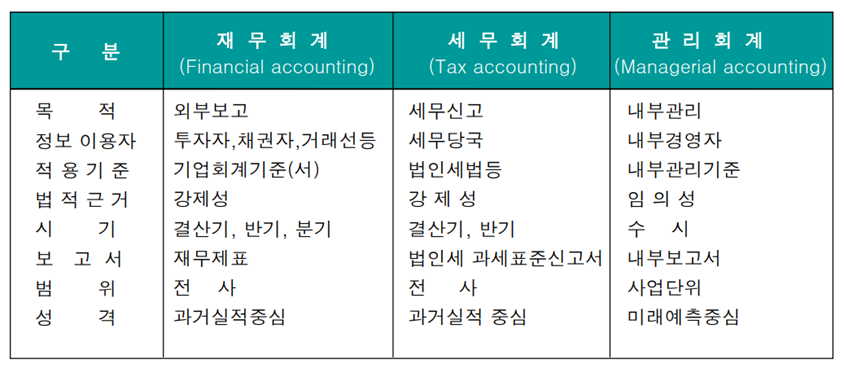

아래에 재무회계, 세무회계, 관리회계의 차이에 대한 비교표가 있다. 작성 대상자가 내부 경영자이고 그 성격이 미래예측 중심이란 측면에서, 경영자가 반드시 해야 할 회계는 관리회계임을 확실히 알 수 있을 것이다.

따라서 관리회계 자료는 세무회계 자료와 다를 수밖에 없다. 외부에 보여주기 위한 것이 아니라 실제적으로 내부에서 일어나는 모든 것을 사실 그대로 포함하기 때문에, 회사의 과거와 현재, 그리고 미래를 예측할 수 있는 근간이 된다. 그렇다면 당연히 사업계획서에 들어가는 것도 관리회계 자료야 할 것인데, 기업 내부적으로 회계를 하지 않고 세무사가 주는 자료만 있다면, 어떻게 올바른 사업계획서를 작성할 수 있겠는가?

따라서 경영자는 실질적인 재무제표(Financial statement)를 보고 경영적 현상을 파악할 수 있어야 한다. 재무제표란 일정기간 경영활동 결과에 따른 일정기간의 경영성과(손익, 현금흐름) 및 일정시점의 재무상태를 나타내는 재무자료를 말한다. 주요 4대 재무제표를 재무상태표(대차대조표), 손익계산서, 이익잉여금처분계산서, 현금흐름표라고 하며, 경영자는 이 네가지 표를 모두 읽고 수치가 이야기하는 행간의 의미를 파악할 줄 알아야 한다.

나는 항상 매년 사업계획서를 작성할 때 가장 기본적으로 손익계산서와 현금흐름표만 포함시켰는데, 이 두가지만 봐도 매출, 비용, 손익, 그리고 자금계획이 모두 포함되기 때문이다. 즉, 내년도 사업계획서를 작성한다면, 재무제표 중 이 두가지 표만 만들어도 모든 사업계획서 목표를 포함하고 있다고 해도 과언이 아닌 것이다.

그러나 많은 중소기업에선 매출목표만 설정하고, 목표를 달성하기 위해 무엇을 하겠다는 막연한 기대감만 가지는 경우가 대부분이다. 유치원 수준의 덧셈과 뺄셈으로 이루어진 손익계산서 하나 제대로 만들지 않고 계획을 세우니, 그 목표가 제대로 달성될 수가 없는 것은 뻔한 일이다.

손익계산서는 경영의 계기판이다. 만약 손익계산서를 매월 보지 않고 경영을 한다면, 자동차를 탈 때 계기판을 전혀 보지 않고 달리는 것과 마찬가지이다. 얼마의 속도로 달리고 있는지, 기름은 여유 있게 남아있는지, 앞으로 목적지까지 얼마나 남아있는지 등을 알아야 목적지까지 제대로 도착할 수 있을 것이다.

이렇듯 손익계산서를 통해 매출과 이익, 비용에 대한 회계적으로 구체화된 수치가 없다면, 적절한 자금예산에 맞게 일을 할 수 없어서, 업무수행은 목표에서 벗어날 수밖에 없는 것이다. 그래서 이번 장에선 가장 기초적인 사업계획서 작성을 위한 재무제표로 손익계산서와 현금흐름표를 이해하고, 이를 통해 자금관리와 사업투자의 경제성분석을 중점적으로 알아보겠다.

—————————-

Financial Statements and Cash Flow Management

In the previous chapter on marketing budgets, I mentioned the advertising budget of Company M, which I had consulted for. What was surprising about Company M at the time was that they handed over all receipts and tax invoices to the tax accountant, and no one in the company paid any attention to financial accounting. Astonishingly, this was a company with 40 billion KRW in revenue, yet it didn’t have a single accounting staff member.

As a result, Company M relied solely on the tax accountant for quarterly VAT filings and year-end financial statements, but these documents merely provided conclusive figures about the past. No one understood how these numbers should guide the future direction of the business. Therefore, I created a five-year PL(Profit & Loss) statement comparison in Excel, allowing the CEO to see trends in revenue, expenses, and profits. After presenting these findings in a clear and organized manner, the CEO was shocked and decided to cut excessive advertising costs.

Relying solely on a tax accountant in this way presents significant management issues. A tax accountant is primarily focused on ensuring that the company complies with tax laws when reporting to the National Tax Service, only handling tax accounting. However, to effectively manage a company, financial accounting and managerial accounting are more important. Relying solely on a tax accountant means that management-oriented accounting is neglected.

Below is a comparison table outlining the differences between financial accounting, tax accounting, and managerial accounting. It becomes clear that the type of accounting managers must focus on is managerial accounting, given that it is intended for internal managers and is primarily future-oriented.

Therefore, managerial accounting data must differ from tax accounting data. Since it includes all the actual occurrences within the company and is not meant for external display, it forms the basis for predicting the company’s past, present, and future. Naturally, the financial data included in a business plan should come from managerial accounting. If a company only has data provided by a tax accountant without conducting its own internal accounting, how can it create an accurate business plan?

Hence, managers must be able to understand the practical financial statements that reveal the company’s management conditions. Financial statements are financial documents that indicate the results of business activities over a certain period, reflecting the company’s performance (profit and loss, cash flow) over that period and its financial position at a certain point in time. The four main financial statements are the balance sheet, PL statement, retained earnings statement, and cash flow statement. Managers must be able to read all four and grasp the meanings hidden between the lines of the figures.

Whenever I create an annual business plan, I always include the PL statement and cash flow statement as a basic requirement, as these two documents alone cover revenue, expenses, profit, and fund planning. In other words, if you are drafting next year’s business plan, simply creating these two financial statements would encompass all the objectives of the business plan.

However, in many small and medium-sized enterprises, only sales targets are set, and there is often a vague sense of expectation regarding what will be done to achieve these targets. It’s no surprise that these targets cannot be achieved without even creating a proper PL statement, which consists of elementary-level addition and subtraction.

The PL statement is the dashboard of management. Managing a business without reviewing the income statement each month is akin to driving a car without looking at the dashboard. To reach your destination safely, you need to know your speed, fuel levels, and how far you have left to go. Similarly, without the concretized figures from an income statement regarding sales, profits, and expenses, you cannot manage your tasks according to an appropriate budget, and your work will inevitably deviate from your goals.

Therefore, in this chapter, we will focus on understanding the PL statement and cash flow statement as the most basic financial statements for drafting a business plan, and through these, we will delve into fund management and the economic analysis of business investments.