손익계산서란 일정기간 동안 기업의 매출과 수익에서 비용을 차감하여 순이익을 나타내는 재무제표이다. 손익계산서는 대부분 많이 접해봤을 것이라 간주하고, 이를 작성하는 방법에 대해서 따로 자세히 설명하진 않겠다.

다만, 경영자 및 관리자가 손익계산서를 통해 반드시 알아야 할 점이 무언인지가 중요한데, 이때 내가 항상 습관적으로 파악했던 것은 숫자 그 자체가 아니라 바로 매출대비 경비율과 이익율이다.

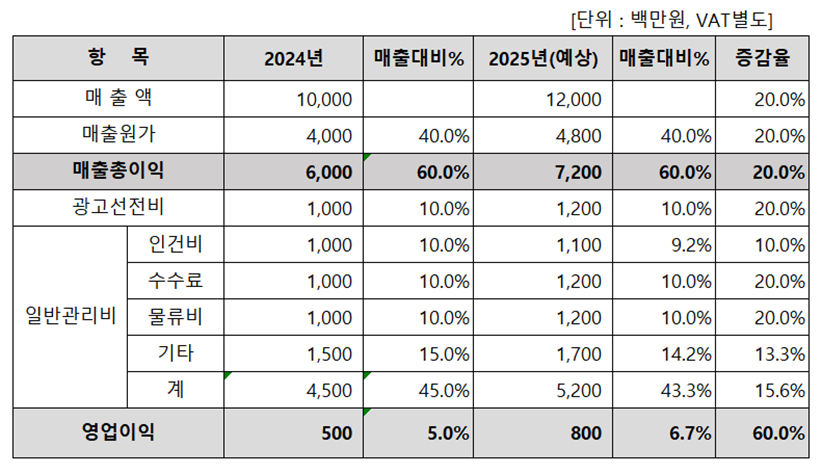

아래 표는 2025년 사업계획 목표를 전년대비 20% 성장하는 계획으로 작성한 간단한 손익계산서 예시이다. 직접적인 영업과 관련성이 적은 영업외비용, 영업외수익과 법인세는 제외하고 영업이익까지만 예를 들었다.

그런데 표를 보면, 2024년과 2025년 모두 금액 우측에 매출대비 퍼센트(%)가 표시되어 있다. 전년대비 비교에서 금액보다 퍼센트를 볼 때 그 의미를 쉽게 파악할 수 있기 때문이다.

먼저 매출총이익율은 60%로 설정했다. 이는 원가율 40%와 관련되어 있다. 일반적으로 화장품업계에서는 원가율 수준을 말할 때 소비자가 대비로 표현을 하는데, 손익계산서 에는 부가세를 제외한 출고가 기준으로 작성하기 때문에 40% 정도로 설정했다. 만약 출고율이 소비자가 대비 50%라면 원가율은 부가세를 감안해서 소비자가 대비 20% 미만일 것이다.

나는 오래전부터 화장품 사업에서 원가율은 최대 40%를 넘지 않아야 한다는 관점을 가지고 있다. 그래야 화장품 시장에서 많은 비용이 들어가는 판관비(판매비 및 일반관리비)를 제외한 영업이익이 흑자로 나타날 수가 있기 때문이다.

물론 회사마다 판매 및 유통구조가 다름에 따라 기준은 달라질 수 있으므로, 경영자는 자신의 회사가 평균적으로 가져가야 하는 원가율, 즉 매출총이익율이 어느 수준인지 기본적으로 파악하고 있어야 한다.

이는 신제품을 개발할 때 제조원가에 대한 즉각적인 판단의 기준이 되며, 유통업체에 제품을 공급할 때도 계산기 두드리지 않아도 되는 마진율에 대한 판단의 근거가 되기 때문이다.

다음으로 비용에 있어서, 판관비의 고정비와 변동비를 구분할 줄 알아야 한다. 이는 손익분기점(BEP-Break Even Point)을 파악하기 위해서도 중요하며, 매출총이익율(60%)에서 이익이 나는 적정 경비수준을 정할 때 매우 중요하다.

일단 변동비란 매출의 증감에 따라 변하는 비용이다. 대표적인 것이 바로 매출원가이다. 매출원가 40%는 매출이 100억이면 40억, 120억이면 48억으로 자동으로 변하기 때문이다. 반대로 고정비는 매출과 상관없이 항상 지출되는 비용이다. 대부분의 일반 관리비들이 이에 속하는데, 그중 인건비, 임대료 등은 매출이 적든 많든 항상 고정적으로 지출되는 비용이다. (계속)

——————————–

The PL statement is a financial statement that shows the net profit by deducting expenses from the revenue and income over a specific period. I assume that most people are familiar with PL statements, so I won’t go into detail about how to prepare one.

However, what’s important is what managers and executives must know when analyzing a PL statement. In this regard, what I have always habitually focused on is not the numbers themselves but rather the expense ratio to sales and the profit margin.

Below is a simple example of a PL statement for the 2025 business plan, which was prepared with the goal of achieving 20% growth compared to the previous year. Indirect operating expenses, non-operating income, and corporate taxes, which are less relevant to direct operations, are excluded, and the example only goes up to operating profit.

In the table, you’ll notice that both 2024 and 2025 figures are accompanied by sales percentages (%) on the right. This is because it is easier to grasp the significance of the comparison year-over-year when looking at percentages rather than absolute figures.

First, the gross profit margin was set at 60%. This is related to a cost ratio of 40%. In the cosmetics industry, the cost ratio is generally expressed in terms of consumer prices, but since the PL statement is prepared based on the ex-factory price excluding VAT, it was set at around 40%. If the ex-factory price is 50% of the consumer price, the cost ratio would be less than 20% when considering VAT.

I have long held the view that in the cosmetics business, the cost ratio should not exceed 40%. This is because, in the cosmetics market, where substantial expenses are incurred in selling, general, and administrative expenses (SG&A), it is only by keeping the cost ratio below 40% that operating profit can be in the black.

Of course, the standard can vary depending on the sales and distribution structure of each company, so managers need to have a basic understanding of the average cost ratio their company should maintain, or in other words, the gross profit margin.

This serves as an immediate benchmark for assessing the manufacturing cost when developing new products and also helps in determining the margin rate without needing to crunch numbers when supplying products to distributors.

Next, when it comes to expenses, it is crucial to differentiate between fixed costs and variable costs within SG&A. This is important not only for determining the break-even point (BEP) but also for setting an appropriate expense level where profit can be made with a gross profit margin of 60%.

Variable costs are expenses that fluctuate with changes in sales. A typical example is the cost of goods sold (COGS). If the COGS is 40%, then when sales are 10 billion, the COGS would automatically be 4 billion, and when sales are 12 billion, the COGS would be 4.8 billion. On the other hand, fixed costs are expenses that are always incurred regardless of sales.

Most general administrative expenses fall into this category, with labor costs and rent being the most common examples of costs that remain constant whether sales are high or low.