내가 최근에 컨설팅을 했던 회사는 디지털 마케팅을 통한 온라인 유통으로 매출 400억원(부가세 별도 기준)을 하고 있는 회사이다. 컨설팅 당시 이 회사는 디지털 마케팅 비용으로 월 4억원(연간 48억원, 매출대비 12%) 정도를 쓰고 있었는데, 온라인 광고비를 전년대비 1억원을 증가시킨 것이지만 매출은 더 이상 성장하지 않고 있었다. 나는 우선 마케팅 예산을 점검했는데, 놀랍게도 400억 매출규모나 되는 회사에 연간 사업계획서가 없었으니 마케팅 예산도 없는 게 당연했다. 오너 한 명의 그때그때 생각과 기분에 따라 광고비가 집행되고 있었기 때문이다.

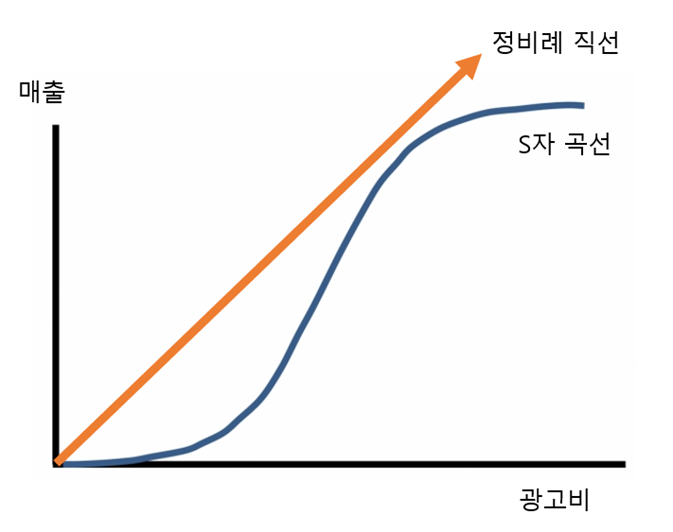

광고비라는 것은 매출과 정비례하지 않는다. 즉, 광고비가 증가할수록 100% 비례해서 매출이 증가하는 것이 절대로 아닌 것이다. 물론 광고비를 많이 투여하면 매출은 증가하겠지만, 어느 정도 수준에 도달하면 점점 매출은 S자 곡선을 그리면서 정체되는 경향이 있다. 따라서 경영자나 마케터들은 S자곡선이 만들어지는 변곡점의 순간을 잘 파악해야 한다.

그래서 나는 이 회사의 5년 동안의 결산자료를 보고 광고비와 매출액의 추이를 파악했다. 5년 전 1억원 수준이었던 광고비는 매년 꾸준히 증가하였고 이와 함께 매출도 증가하였지만, 2년 전인 2021년부터 매출은 400억원 수준에서 머물고 있었던 것이다. 그래서 광고비를 더 늘렸지만 별 소용이 없었고, 영업이익도 감소하는 추세였다.

그래서 나는 5년간 비교분석 자료를 CEO에게 보여주며, 적정 마케팅 예산을 월 최대 3억원으로 제안했다. 연간 36억원으로 매출액 대비 9% 예산이었다. 여기서 중요한 점은 월 3억원이라는 금액이 아니라, 매출대비 9%라는 비율이다. 즉, 9% 예산은 매출이 증가하면 광고비 금액이 증가할 수도 있고, 매출이 감소하면 광고비도 감소할 수도 있도록 탄력적으로 운영해야 하기 때문이다.

기업은 기본적으로 이익이 나야 지속적인 운영이 가능하다. 따라서 CEO는 회사를 운영하는데 필요한 적정 이익수준을 항상 염두해두고 비용을 관리해야 하는데, 대부분 중소기업 CEO들은 얼마의 금액수준으로만 어렴풋이 감으로 판단하는 경우가 많다. 하지만 중요한 것은 매출액대비 비율(%)임을 명심해야 한다. 그래서 나는 손익계산서의 가장 오른쪽에 경비율(%)을 표시하게 하고, 매월 %의 변화 추이를 보는 습관을 만들었다. 그렇게 보면 평소와 다름없이 같은 금액의 비용이 지출 되었더라도 다른 점을 발견할 수 있기 때문이다.

내가 많은 중소기업 CEO들과 얘기를 나누고 자문을 했을 때 가장 큰 문제점으로 느꼈던 건, 대부분이 사업계획을 하지 않고 있으며 가장 기초적인 회계지식도 없다는 것이다. 최소한 재무상태표, 손익계산서, 현금흐름표 정도는 매월 작성을 하도록 해야 하고, 경영자들은 그걸 습관적으로 검토하고 숫자가 말하는 의미를 파악하여 경영활동에 적용해야 한다. 그럼에도 불구하고 회계자료를 통째로 세무사에 넘기고, 나중에 조정된 회계결산 자료만 보고 이익이 난다는 것으로 오해한다면 큰 낭패를 당하기 쉽다. 이점에 대해서는 뒤에 따로 경영관리 질문에서 이야기해보고자 한다.

———————-

The company I consulted for recently was making 40 billion won in revenue (excluding VAT) through online distribution via digital marketing. At the time of the consultation, they were spending about 400 million won per month (4.8 billion won annually, 12% of revenue) on digital marketing. Although they increased their online advertising budget by 100 million won compared to the previous year, their revenue had not grown further. Surprisingly, a company with a 40 billion won revenue scale did not have an annual business plan, so it was natural that they had no marketing budget. The advertising costs were executed according to the owner’s thoughts and moods at the time.

Advertising costs do not directly correlate with revenue. In other words, it’s not that as advertising expenses increase, revenue increases 100% proportionally. Of course, if you invest a lot in advertising, revenue will increase, but at some point, revenue tends to stagnate and follow an S-curve. Therefore, business owners and marketers need to be aware of the inflection point where the S-curve is created.

So, I reviewed the company’s financial statements for the past five years and analyzed the trends in advertising expenses and revenue. Five years ago, the advertising budget was around 100 million won, which had been steadily increasing annually, along with revenue. However, from 2021, two years ago, revenue remained at 40 billion won. Increasing the advertising budget further was futile, and operating profits were declining.

I presented the five-year comparative analysis data to the CEO and proposed an appropriate marketing budget of up to 300 million won per month. That would be 36 billion won annually, or 9% of revenue. The important point here is not the amount of 300 million won per month, but the ratio of 9% relative to revenue. This is because a 9% budget means that the advertising amount can increase if revenue increases, and decrease if revenue decreases.

A business fundamentally needs to make a profit for sustainable operation. Thus, the CEO must always keep in mind the necessary profit level for running the company and manage costs accordingly. Most small and medium-sized enterprise CEOs only vaguely judge by the amount of money. However, it’s crucial to remember that it’s the percentage of revenue that matters. That’s why I made it a practice to display the expense ratio (%) on the far right of the income statement and to habitually monitor the % changes monthly. This way, even if the same amount of expenses were incurred as usual, one could notice differences.

When I talked to many small and medium enterprise CEOs and advised them, the biggest problem I felt was that most of them do not make a business plan and lack even the most basic accounting knowledge. At the very least, financial statements, income statements, and cash flow statements should be prepared monthly, and business owners should habitually review them to understand the numbers and apply them to business activities. Otherwise, if you hand over the accounting data entirely to the accountant and later only see the adjusted accounting settlement data thinking that a profit has been made, you could be greatly mistaken. I’ll talk about this management issue separately later.