소비자의 무지와 회사의 상술

일반적으로 보험상품은 장기 상품이어서 한 번 가입하면 오랫동안 유지해야 합니다. 따라서 회사로서는 장기적으로 꾸준히 유입되는 자금을 운용할 수 있다는 잇점이 있습니다.

그것에 착안한 어느 정부가 각 가정에 묻혀있던 돈을 금융권으로 끌어들이기 위해 보험회사를 만들었습니다. 그리고 판매원을 모집하지요. 그들에게 대략의 상품 특성을 설명해 주고는 이 상품을 팔아 오면 수수료 (원래는 기여에 대해 지급하는 Compensation입니다.)를 지급한다고 이야기합니다.

판매원들은 전문적 영업사원이 아니고 따라서 아는 사람들에게 찾아가 홍보하기 마련입니다. 그런데 그 아는 사람들의 하나같은 요구사항이 재미있습니다.

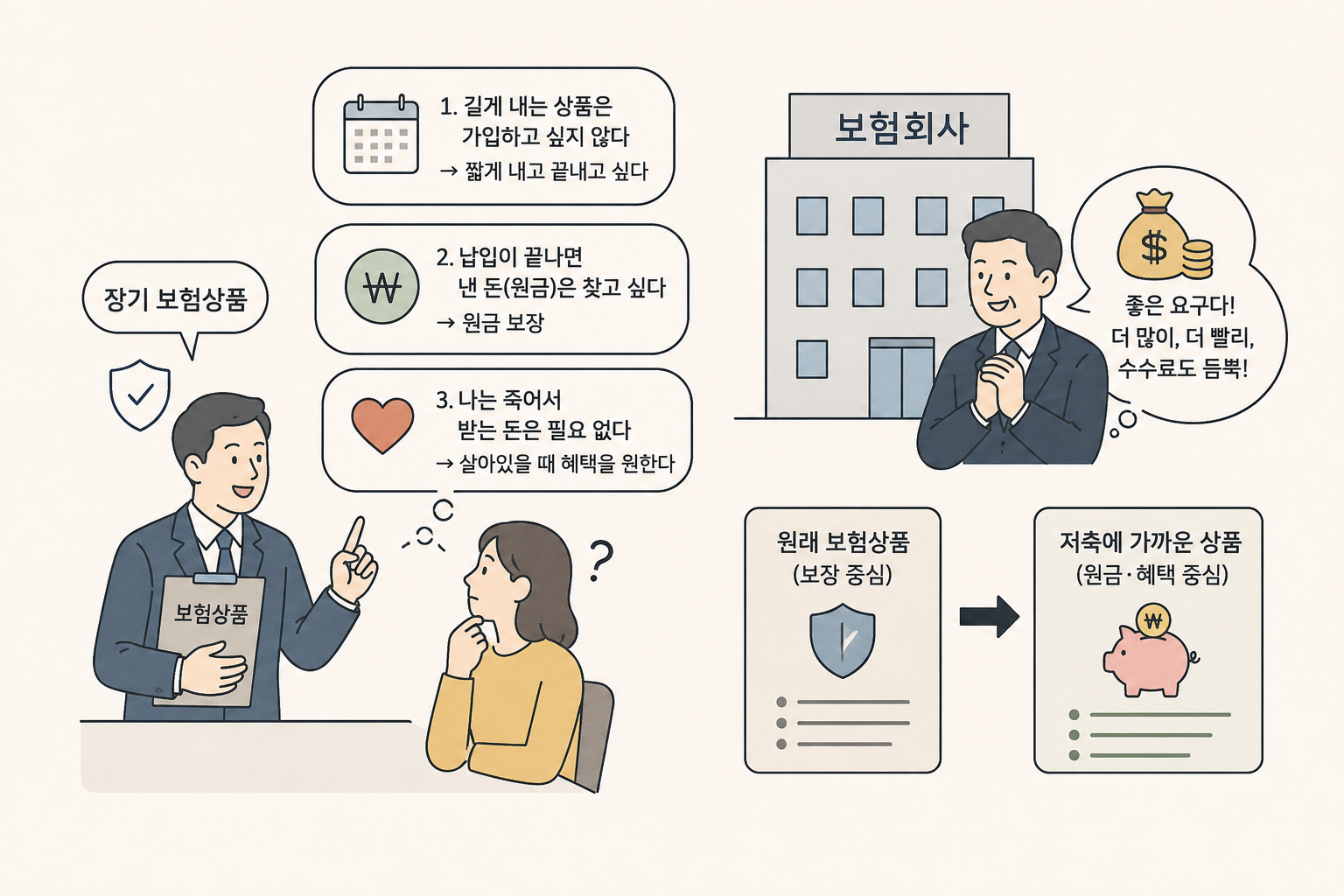

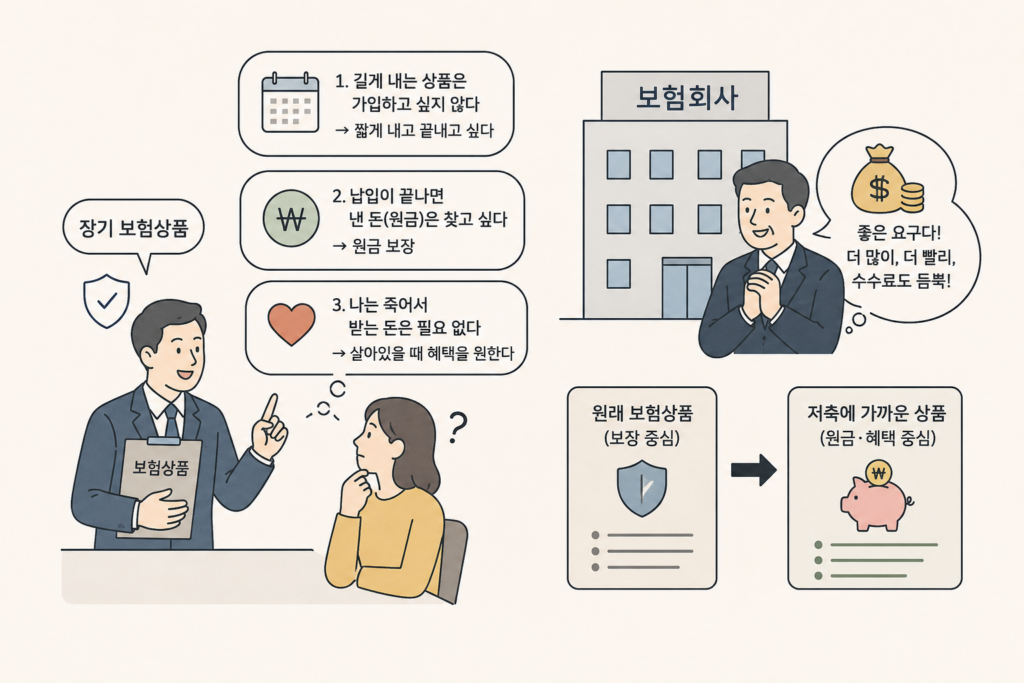

첫째 나는 길게 내는 상품은 가입하고 싶지 않다.

고객은 보험료의 납입을 짧게 내고 끝내고 싶답니다.

보험은 장기간 거래해야 하는 상품인데 소비자는 긴 납입을 부담스러워합니다.

둘째 납입이 끝나면 낸 돈의 원금은 찾고 싶다.

고객은 어떤 경우에 보장이 되고 얼마가 보장되는 지에 대한 것은 잘 모르겠고, 하여간 보험의 기간이 끝나면 낸 돈은 돌려받았으면 한다.

통상 위험보험료는 돌려받지 못하는 돈이고 나중에 원금을 돌려받으려면 저축보험료를 추가로 더 내야 하고 이렇게 납입하는 보험료가 늘어나면 보험료에 비례하여 책정하는 부가보험료도 늘어나게 마련입니다.

소비자는 자신에게 필요한 것 보다 더 많은 돈을 보험회사에 맡기고 싶고, 더 많은 돈을 보험회사에 월급으로 주겠다고 이야기합니다.

셋째 나는 죽어서 받는 돈은 필요 없다.

고객은 살아있을 때 혜택을 받는 보험이 좋다고 합니다.

보험회사를 거래하는 목적은 갑작스럽게 내가 대비할 수 없을 만큼 큰 위험이 발생했을 때를 그 위험을 보험회사로 넘기는 상품입니다. 오히려 충분히 부담할 수 있는 정도의 손실은 보험보다는 저축으로 만드는 것이 더 효과적일 텐데 소비자는 큰 위험은 본인이 부담하고 작은 위험을 보험회사에 맡기겠답니다.

고객이 요구하는 사항은 하나같이 장기 보험상품이 아닌 단기 저축상품에 적용되어야 하는 사항들인데, 이런 이유로 판매에 실패한 영업사원들이 회사에 와서 상품 좀 제대로 만들어 달라고 하소연을 합니다.

보험회사는 고객의 이런 요구가 너무 좋습니다. 왜냐하면 회사입장에서는 오랫동안 조금씩 받아야 하는 보험료를 고객이 더 빨리 더 많이 주겠다고 하는 데다가 수고비를 듬뿍 얹어 주겠다는 이야기이니까요.

그래서 보험회사가 원래의 보험상품이 아닌 저축에 가까운 상품을 만들기 시작합니다. (계속)

————-

Consumer Ignorance and Corporate Sales Tactics

In general, insurance products are long-term financial products that should be maintained for an extended period once purchased. From the insurer’s perspective, this provides the advantage of being able to manage a steady inflow of long-term funds.

Recognizing this, a certain government established insurance companies as a way to attract idle household funds into the financial system. Sales agents were then recruited and given a basic explanation of the product features, along with the promise of commissions—originally intended as compensation for contribution—if they successfully sold the products.

Most sales agents were not professional financial advisors, so they naturally approached acquaintances and people within their personal networks. Interestingly, the requests from those potential customers were remarkably similar.

First, “I do not want to enroll in a product that requires long-term payments.”

Customers wanted to finish paying premiums within a short period.

However, insurance is fundamentally a product designed for long-term transactions, while consumers tend to view long payment periods as burdensome.

Second, “Once the payment period ends, I want my principal back.”

Most customers are not particularly interested in understanding the details of coverage or payout conditions. They simply want to recover the money they paid once the insurance term ends.

In reality, the risk premium is generally non-refundable, and recovering the principal later requires paying additional savings premiums. As total premiums increase, the loading premium—calculated proportionally to the premium amount—also increases.

In effect, consumers voluntarily choose to entrust more money than necessary to insurance companies while simultaneously agreeing to pay the company higher operating compensation.

Third, “I do not need money after I die.”

Customers prefer insurance products that provide benefits while they are alive.

The fundamental purpose of insurance is to transfer catastrophic risks—those too large for an individual to handle alone—to the insurance company. In many cases, losses that are manageable would be more effectively handled through savings rather than insurance. Yet consumers often choose to retain large risks personally while transferring relatively small risks to insurers.

The demands customers make are more appropriate for short-term savings products than for long-term insurance products. As a result, sales agents who struggled to sell traditional insurance products returned to their companies asking for products that customers would actually want to buy.

Insurance companies welcomed these demands enthusiastically. From the company’s perspective, customers were volunteering to pay premiums more quickly and in larger amounts than originally necessary, while also offering generous compensation through higher loading premiums.

As a result, insurance companies gradually began creating products that resembled savings instruments more than traditional insurance products. (To be continued)