회수기간법(PBP)은 매년 현금 유입액의 누계가 최초 투자액과 같아질 때까지의 기간, 즉 최초 투자액을 회수하는데 걸린 기간으로 투자를 평가하는 방법이다.

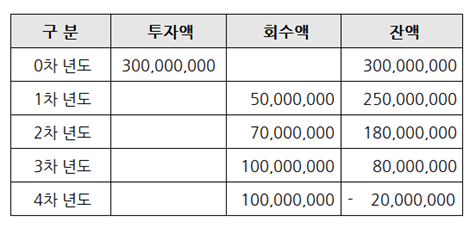

예를 들면, 아래 표는 초기 투자액 3억원이 최종 회수될 것이라 예상되는 기간을 표시한 것이다. 회수액은 당연히 손익계산서 상의 수치가 아니라, 현금으로 들어오는 현금흐름표 기준으로써, 아래 표에선 4차년 중간에 회수되는 걸로 나왔다.

내가 미니골드 주얼리 회사에서 신규사업팀장으로 있었던 2005년만 해도, 신규사업 투자 결정을 할 때 고려했던 것은, 5개년 손익과 투자금액이 몇 년 차에 회수될 수 있는 지(PBP)였다. 당시 미니골드에선 PBP를 만 3년으로 설정하고, 3년 내로 투자원금이 회수되지 않으면 신규사업을 할 수 없다는 의사결정을 하였다.

주로 현금성 자산인 금을 다루던 기업이었기 때문에, 투자금 회수기간도 빠른 편이었다. 하지만 이런 평가는 이미 두가지 실수를 한 것이다. 첫째 손익이 아니라 현금흐름으로 했어야 하며, 둘째 PBP만으론 투자금의 기회비용을 반영할 수 없기 때문이다.

그렇다면 화장품 사업에선 PBP가 어느 정도일까? 주요 소비재 제품인 화장품 사업에서는 신규 브랜드 투자에 대해선 주로 3~5년의 PBP를 책정하는 경우가 많다. 그러나 PBP는 투자의 성격이나 자기자본이나 차입금의 수준에 따라, 기업마다 달라진다.

만약 차입금이 많고 이자부담이 크다면 목표 PBP도 짧게 설정해야 할 것이다. 따라서 만약 PBP 기준이 3년이라면, 위 예시의 투자는 하면 안된다. 이처럼, PBP를 하는 이유는 투자금 회수기간이 길면 길수록 위험도 높아지기 때문에, 미래의 위험을 방지할 수 있는 중요한 의사결정의 기준이 된다.

———————

The Payback Period (PBP) method is an investment evaluation method that measures the period required to recover the initial investment amount, i.e., the time it takes for the cumulative cash inflows each year to equal the initial investment.

For example, the table below shows the period in which the initial investment of 300 million KRW is expected to be fully recovered. The recovery amount, of course, is not based on figures from the income statement but rather on the cash inflows as per the cash flow statement. In the table below, the recovery is shown to occur in the middle of the fourth year.

When I was the head of the new business team at the Mini Gold jewelry company in 2005, one of the key considerations when deciding on a new business investment was the projected PBP, which indicated in which year the investment amount could be recovered.

At that time, Mini Gold had set the PBP at a maximum of three years, meaning that if the initial investment could not be recovered within three years, the new business would not be pursued. Since the company primarily dealt with cash-equivalent assets like gold, the investment recovery period was relatively short.

However, this approach involved two fundamental mistakes. First, the evaluation should have been based on cash flow, not profit and loss. Second, relying solely on PBP fails to account for the opportunity cost of the investment.

So, what would the PBP be in the cosmetics industry? For major consumer goods like cosmetics, it is common to set a PBP of 3 to 5 years for new brand investments.

However, the PBP varies by company depending on the nature of the investment and the levels of equity and debt. If a company has a high level of debt and significant interest burdens, the target PBP should be set shorter.

Therefore, if the PBP criterion is set at 3 years, the investment in the example above should not be made. The reason for using PBP as an evaluation metric is that the longer the investment recovery period, the higher the associated risk, making it an important decision-making criterion for mitigating future risks.