“신제품 개발 시 시장에서 경쟁할 수 있는 가격 설정의 중요성을 강조합니다. 우수한 제품이라도 너무 높은 원가로 인해 경쟁력을 잃지 않도록, 타깃 코스팅을 통한 적정 원가 산정과 가격 결정 과정을 소개하며, 경쟁적인 가격전략을 통해 제품의 성공 가능성을 높이는 방법을 공유합니다.”

“Emphasizes the importance of setting competitive prices during new product development. To ensure that even superior products do not lose their competitiveness due to too high costs, it introduces the process of determining the appropriate cost and deciding on prices through target costing, sharing methods to increase the likelihood of product success through competitive pricing strategies.”

막상 우수한 신제품을 개발했는데, 원가가 너무 높아서 가격이 비싸지는 바람에 시장에서 경쟁력이 없어진다면 어떻겠는가? 그 동안 고생 끝에 개발한 신제품이 시장에서 받아들일 수 없는 가격으로 출시되어야 한다면, 그 제품은 출시 전부터 이미 실패한 것이나 다름없다.

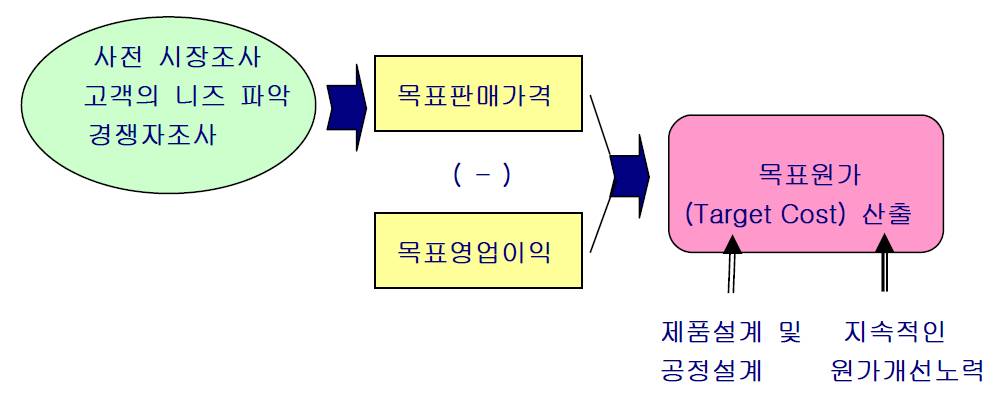

그래서 제품을 개발하기 전에 시장에서 경쟁력 있는 가격을 먼저 책정하고, 그 가격에 맞는 제품이 개발되어야 할 것이다. 따라서 회사에 이익이 나면서도 경쟁력 있는 가격을 만들기 위해서는 제품을 개발하기 전에 적정한 원가를 미리 책정해서 제품이 만들어져야 하는데, 이런 방법을 타깃 코스팅(Target Costing) 또는 목표원가 책정이라 한다.

신제품 개발 단계에서 가격책정(Pricing)은 신제품의 승패를 좌우할 정도로 매우 중요함에도 불구하고, 많은 경영자들이 간과하고 넘어가는 것이 타깃 코스팅(Target Costing)이다. 타깃 코스팅이란 전통적인 가격결정방식인 개발된 제품의 제조원가를 기준으로 기업의 이익을 더하여 판매가격을 결정하는 방식과 반대로, 제품개발 이전에 판매가격을 결정하고 역으로 목표원가를 먼저 설정하는 방식이다. 즉, 사전 시장조사를 통해 고객의 니즈와 경쟁제품의 정보를 파악하여 경쟁적 우위라 판단되는 판매가격(Target Price)을 먼저 산출한 후에, 기업에서 요구하는 영업이익(Target Profit)과 예상비용들을 빼서 제품의 원가(Target Cost)를 설정하고, 그 원가에 맞게 제품이 개발되도록 하는 방식이다.

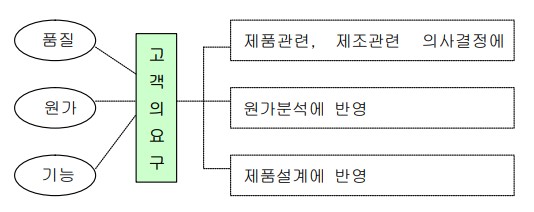

그리하여 경쟁력 있고 소비자가 수용할 수 있는 가격대가 선정되면, 비로소 회사가 기본적으로 가져가야 할 적정 원가기준 내에서 제품의 기능과 효과가 나올 수 있도록 개발이 가능한지 검토한 후, 신제품 개발이 시작되어야 한다. 그래서 타깃 코스팅은 품질, 원가, 기능성(Quality, Cost, Functionality)이 조화를 이루는 경쟁전략이라고 할 수 있다.

특히 작은 기업에서 B화장품을 개발했던 내 경우에도, 타깃 코스팅은 더욱 더 중요했다. 나는 중국 온라인 시장에서 제품을 팔겠다는 목표로 판매가를 설정했는데, 중국 온라인/모바일 유통 판매가는 일단 100위안 이상은 경쟁력이 없다고 생각했다. 그래서 할인율 20~30%를 감안해서 한국 소비자가를 22,500원 수준으로 책정하였다. 당시 위안화 환율 180원 기준으로 중국 소비자가 125위안인 것이다. 따라서 상시 할인가(20~30%)는 100~88 위안 수준이 된다.

다음으로 수출 유통마진을 고려한 수출가는 소비자가 22,500원 대비 25%인 5,625원(부가세별도 5,114원)으로 책정하였다. 따라서 여기서 회사의 마진율을 감안한 제반 비용을 차감하면 목표원가가 나오게 된다. 실제로 대부분 화장품 브랜드는 품목에 따라 목표원가보다 높은 원가도 있고 낮은 원가도 있어서, 평균적으로 우리가 원하는 목표원가 수준에 맞춰서 개발하면 된다.

이처럼 신제품 개발을 할 때, 제품 중심적인 생각으로 일단 기능이 뛰어난 우수한 제품부터 개발하자는 생각에서 벗어나, 어떤 소비자에게 어떤 유통에서 팔 것인지부터 결정하고, 그 유통에서 경쟁자들과 치열하게 싸워도 회사에 적정 이익을 줄 수 있는 목표원가를 책정하는 타깃 코스팅을 먼저 고려하는 습관이 필요하다.

그러기 위해서는 아래와 같은 절차가 습관적으로 이루어져야 한다. 그렇다면 효율적인 타깃 코스팅을 통해 경쟁적 제품개발이 가능할 것이다.

① 목표 판매가격의 결정: 시장분석, 제품전략 수립, 경쟁력 있는 가격설정.

② 목표 영업이익의 결정: 과거 실적, 경비 분석, 이익계획.

③ 허용가능 목표원가의 결정: 제품개발 가능성 검토.

④ 원가절감 목표: 제품설계, 개발기간 단축, 생산 효율성.

⑤ 효율적 비용관리: 광고판촉비 예산, 물류비 효율성

————————

Imagine developing an outstanding new product, only to find its cost so high that the market price renders it uncompetitive. The effort poured into creating such a product would feel wasted if it had to be launched at an unacceptably high price, essentially dooming it before it even hits the market.

To avoid such scenarios, it’s crucial to set a competitive market price before the product development begins. Achieving a price that is both competitive and profitable necessitates establishing a target cost early in the development process. This approach, known as target costing or target cost management, flips the traditional pricing method on its head. Rather than determining the selling price based on the cost of production plus a desired profit margin, it starts with a competitive price point, deducts the desired profit, and then sets the target cost.

Despite the critical importance of pricing in new product development, target costing often gets overlooked by many executives. It’s a strategy that contrasts traditional cost-plus pricing, focusing instead on working backwards from a market-based price point to ensure the product can be produced at a cost that ensures profitability.

Target costing involves a comprehensive review of a product’s potential performance, cost, and functionality to determine if it can be developed within a certain cost framework. It’s a competitive strategy that harmonizes quality, cost, and functionality, ensuring the product meets market expectations at a feasible cost.

Especially for smaller companies, like the one I developed cosmetic B for, targeting the Chinese online market, target costing was crucial. I aimed for a retail price that would be competitive in China’s online/mobile commerce environment, considering a market price below 100 yuan as non-competitive. Thus, setting the Korean retail price at 22,500 won, considering the exchange rate and a discount rate of 20-30%, resulted in a target consumer price in China.

Considering export margins and company profit margins, the target cost was calculated. This methodology not only ensures that the product is developed within the desired cost parameters but also highlights the importance of starting the development process with a clear understanding of the target market and pricing strategy.

To effectively implement target costing, companies must adopt a disciplined approach that includes determining the target selling price, target profit margin, and allowable target cost, followed by setting cost reduction goals and managing expenses efficiently.

This strategic focus ensures that product development aligns with market demands and financial objectives, facilitating competitive product development.

1) Determination of the target selling price: Market analysis, product strategy development, setting a competitive price.

2) Determination of the target operating profit: Analysis of past performance, cost analysis, profit planning.

3) Determination of the allowable target cost: Review of product development feasibility.

4) Cost reduction goals: Product design, shortening of development period, production efficiency.

5) Efficient cost management: Budget for advertising and promotion, efficiency of logistics costs.